Key Takeaways

- Identity fraud in real estate has surged 30%, and FinCEN’s 2026 Residential Real Estate Reporting Rule now requires reporting for non-financed transfers to entities or trusts.

- Florida CAMs must use Customer Identification Programs with biometric verification, OFAC and PEP screening, transaction monitoring over $3,000, and SAR filing to avoid fines up to $1 million.

- Core practices include staff training on red flags such as structuring payments and third-party rent, plus FCRA-compliant background checks with clear adverse action notices.

- Automated document redaction, ongoing tenant monitoring, and community-specific compliance programs use analytics to deliver risk insights and complete audit trails.

- TenantEvaluation’s IDVerify platform delivers biometric KYC, FCRA screening, and about 70% time savings for Florida CAMs, so get started today for fraud-resistant compliance.

Florida Compliance Landscape for 2026 CAM Operations

The March 1, 2026 FinCEN rule requires reporting for all residential real estate transfers where buyers are legal entities or trusts, with no minimum price threshold. Florida-specific updates include FARBAR contract changes that require buyer information disclosure before closing. The Florida Information Protection Act (FIPA) sets strict data privacy protections, while the FCRA governs tenant screening reports that cover credit, eviction, criminal history, and OFAC watchlists. CAMs who manage HOAs and condominiums face manual document reviews, higher identity fraud exposure, and slow approval processes that delay revenue.

11 KYC/AML Best Practices for Florida Property Managers

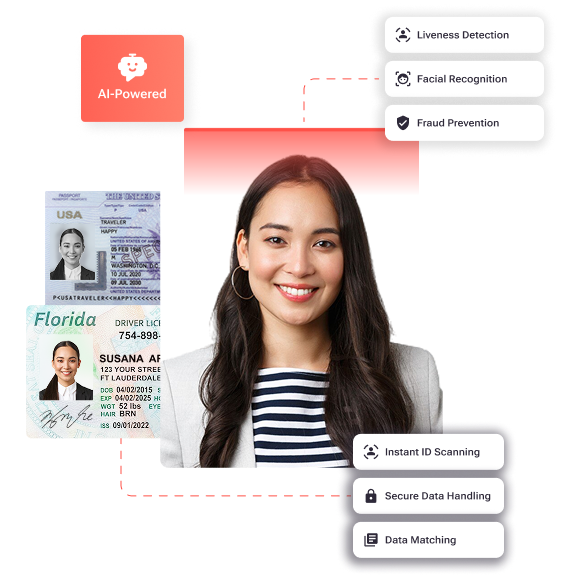

1. Build Customer Identification Programs with Biometric Verification

Florida CAMs need CIP protocols that require government-issued ID validation, address verification, and biometric confirmation. Modern KYC onboarding flows combine ID document capture with selfie liveness checks and finish verification in under 2 minutes. TenantEvaluation’s IDVerify combines government ID authentication, AI-powered liveness detection, and facial biometric matching inside the screening workflow, which removes third-party redirects and keeps FCRA compliance intact.

2. Run OFAC and PEP Screening on Every Applicant

Property managers should screen every applicant against Office of Foreign Assets Control (OFAC) sanctions lists and Politically Exposed Persons (PEP) databases. KYC providers support watchlist screening that covers OFAC, EU, and UN sanctions along with PEP status checks. Florida CAMs need to document all screening results and maintain audit trails for regulators. TenantEvaluation’s screening covers nationwide and global background checks, including criminal records, offenses registries, and FBI Most Wanted, while following FCRA-compliant procedures.

3. Anchor AML Programs on the Five Core Pillars

Effective AML programs for CAMs rely on five pillars: risk assessment, Customer Due Diligence (CDD), transaction monitoring, suspicious activity reporting, and ongoing training. Teams should run risk assessments on customers and transactions to spot AML risks and use monitoring systems to detect unusual activity. Florida property managers can then tailor risk profiles by community demographics, rental amounts, and payment patterns.

4. Track Transactions Above the $3,000 Threshold

CAMs should track all cash transactions, rent payments, and deposits over $3,000 for money laundering indicators. Real-time monitoring tools with data mining algorithms help analyze transactions and highlight suspicious behavior patterns. Florida CAMs can set automated alerts for structured payments, unusual payment sources, and frequent large cash deposits that signal possible laundering.

5. Train Staff to Spot and Escalate Red Flags

Property management teams need training to recognize suspicious activities such as structuring transactions, unusual payment methods, PEP connections, and inconsistent applicant information. Clear procedures for reporting and escalating suspicious transactions or red flags keep responses consistent. Common red flags include cash payments from third parties, reluctance to provide identification, and applicants with addresses in high-risk jurisdictions.

|

Red Flag Indicator |

Description |

CAM Action Required |

|

Structuring Payments |

Multiple payments under $3,000 to avoid reporting |

Document pattern, file SAR if activity appears suspicious |

|

Third-Party Payments |

Rent paid by unrelated individuals |

Verify relationship and source of funds |

|

PEP Connections |

Applicant linked to politically exposed persons |

Apply enhanced due diligence and ongoing monitoring |

|

High-Risk Jurisdictions |

Addresses or payments from sanctioned countries |

Run OFAC screening and consider application denial |

|

Inconsistent Information |

Mismatched ID details or employment data |

Request additional verification and investigate for fraud |

6. Automate Secure Document Collection and Redaction

Automated systems for secure document collection, PII redaction, and compliance documentation reduce manual risk. TenantEvaluation’s platform automatically redacts Social Security numbers, banking details, and other sensitive data while maintaining PCI Level 1 compliance and end-to-end encryption. Florida CAMs lower liability exposure and simplify audit preparation with this automated document management.

7. Follow FCRA Rules for Background Screening

The FCRA governs Florida tenant screening reports that include credit, eviction, criminal history, sex offender registry, and OFAC watchlists. Property managers must use consistent screening criteria, issue adverse action notices, and confirm permissible purpose for every credit check. TenantEvaluation operates as a direct credit bureau reseller and provides built-in adverse action workflows with an FCRA-first design.

8. Create Clear SAR Filing Procedures

Prompt reporting procedures for suspicious transactions with defined escalation paths keep CAMs aligned with AML rules. Florida CAMs should file SARs within 30 days of detecting suspicious activity and keep detailed documentation and investigation notes. Teams should follow written procedures with documented reasoning for alerts and risk ranking for prioritization.

9. Use Ongoing Tenant Monitoring for Risk Signals

CAMs need processes to investigate flagged transactional activity so they can respond quickly to suspicious behavior. Monitoring rent payment patterns, lease violations, and behavioral changes helps uncover money laundering or fraud. Dashboards and reports that track fraud metrics such as delinquencies make risk trends easier to spot.

10. Tailor Compliance Programs to Each Community

Compliance programs work best when they match each community’s risk profile, demographics, and regulatory exposure. High-value condominiums often require enhanced due diligence compared with standard rental properties. TenantEvaluation’s platform lets Florida CAMs configure custom screening criteria, document requirements, and approval workflows for each community association while keeping consistent compliance standards.

11. Turn Analytics into Actionable Risk and Compliance Insights

Teams should track metrics such as alert volumes, false-positive rates, investigation times, and SAR filings to measure performance. Complete activity logs and audit trails that record actions, document changes, and timestamps support compliance oversight. TenantEvaluation provides analytics on community demographics, risk patterns, and compliance metrics that guide strategic decisions.

Schedule a demo today to see how TenantEvaluation streamlines KYC and AML compliance for Florida property managers.

Why TenantEvaluation Fits Florida CAM Compliance Needs

TenantEvaluation launched in 2007 specifically for Florida Community Association Managers and delivers a resident screening and onboarding platform that treats FCRA compliance as the foundation. IDVerify offers biometric identity verification with government ID validation, AI-powered liveness detection, and facial matching inside the screening workflow. QuickApprove gives Boards of Directors real-time application review and voting tools that generic screening platforms do not provide.

TenantEvaluation serves more than 5,000 communities and processes about 100,000 applications each year while maintaining a 4.8/5 Google rating and generating $150 million for client communities. The platform holds PCI Level 1 compliance and delivers up to 70% time savings compared with manual processes. As a direct TransUnion and Equifax reseller, TenantEvaluation provides legitimate credit data access under strict bureau rules and shields associations from added liability.

|

Feature |

TenantEvaluation |

ApplyCheck |

Verify Screening |

Manual Process |

|

Processing Time |

5-10 minutes |

2-5 days |

2-5 days |

5-10 days |

|

Biometric Verification |

Native IDVerify |

Third-party redirect |

Document only |

Visual inspection |

|

Board Dashboard |

QuickApprove included |

Not available |

Not available |

Email and phone |

|

FCRA Compliance |

Built-in foundation |

Basic compliance |

Basic compliance |

Manual tracking |

RealManage, a leading TenantEvaluation partner, saved $240,000 per year by removing 50 hours of daily manual processing and cutting approval times by 50%. The automated platform removes paper-based risks and applies bank-level data encryption to protect sensitive resident information.

Implementation Checklist and Red Flag Reference for CAMs

KYC and AML Implementation Checklist for Florida CAMs:

- Establish a Customer Identification Program with biometric verification.

- Configure OFAC and PEP screening for every applicant.

- Set up transaction monitoring for payments above $3,000.

- Train staff on red flag recognition and escalation procedures.

- Use automated document collection and PII redaction.

- Maintain FCRA-compliant background screening processes.

- Define SAR filing procedures and documentation requirements.

- Deploy ongoing tenant monitoring and risk assessment.

- Customize compliance programs for each community risk profile.

- Configure analytics dashboards for compliance reporting.

- Schedule regular compliance training and system updates.

Schedule a demo today to apply these best practices with TenantEvaluation’s automated compliance platform.

Frequently Asked Questions

What is KYC compliance for Florida property managers?

KYC compliance for Florida property managers means running Customer Identification Programs that verify tenant identities with government-issued ID validation, address confirmation, and biometric verification. Under the 2026 FinCEN rules, property managers must collect beneficial ownership information for entity buyers and keep detailed records for regulators. KYC requirements also include OFAC screening, PEP verification, and ongoing monitoring of tenant activities to reduce money laundering and fraud.

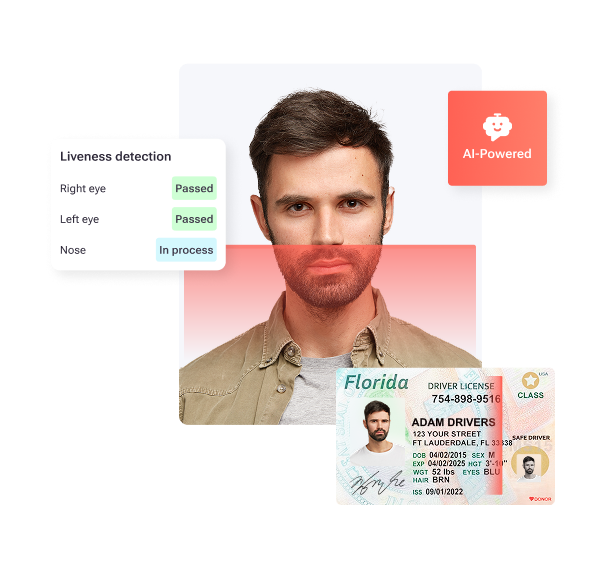

How does IDVerify+ support AML compliance for community associations?

IDVerify+ supports AML compliance by adding biometric identity verification that confirms applicant authenticity before approval decisions. The system validates government-issued IDs, performs AI-powered liveness detection, and runs facial biometric matching to block identity fraud and synthetic identity schemes. This biometric layer aligns with FCRA workflows and creates audit-ready documentation for regulators, which moves communities from document-only checks to verified physical identity confirmation.

What is the SAR filing threshold for Florida property managers?

Florida property managers must file Suspicious Activity Reports for transactions that involve $3,000 or more in cash when they detect suspicious activity. Covered activity includes structured payments that avoid reporting thresholds, unusual payment sources, and transactions that involve politically exposed persons or sanctioned jurisdictions. CAMs must file SARs within 30 days of detecting suspicious activity and keep detailed documentation that supports the filing decision.

How do 2026 FinCEN rules change Florida CAM workflows?

The March 1, 2026 FinCEN Residential Real Estate Reporting Rule requires Florida CAMs to collect and report beneficial ownership information for all residential transfers to legal entities or trusts, regardless of purchase price. CAM workflows now include extra buyer documentation, longer preparation timelines, and earlier identification of entity purchases. Florida-specific FARBAR contract updates also require buyer information disclosure before closing and assign reporting costs to buyers.

What are the key differences between KYC and AML for property managers?

KYC focuses on customer identification and verification through Customer Identification Programs, government ID validation, and biometric confirmation to establish tenant identity. AML covers broader transaction monitoring, suspicious activity detection, OFAC screening, and regulatory reporting that target money laundering schemes. KYC establishes who the customer is, while AML tracks what the customer does through ongoing transaction surveillance, red flag detection, and SAR filing for suspicious patterns or high-risk activities.

Conclusion: Turning Compliance into a Repeatable Process

These 11 KYC and AML best practices give Florida property managers a clear framework to meet 2026 FinCEN requirements, FCRA obligations, and rising identity fraud risks. TenantEvaluation’s specialized platform automates these steps while keeping strict compliance standards, which lets CAMs focus on community management instead of manual verification work. Schedule a demo today to upgrade your compliance operations with automation designed for Florida community associations.