Key Takeaways for VA Condo Buyers and Florida HOAs

- Use the official VA Condo Report at https://lgy.va.gov/lgyhub/condo-report to verify Florida condo approvals by state, city, and development name.

- Confirm that the status shows “Accepted Without Conditions” or “Accepted With Conditions,” and check again during escrow because approvals can change.

- Expect Florida-specific hurdles such as HOA rental restrictions, high investor concentrations, insurance volatility, and low owner-occupancy rates that block many approvals.

- Recognize that major cities like Miami, Tampa, Orlando, and Jacksonville offer different VA-approved options, so focus on financially stable HOAs with clear leasing rules.

- Florida HOAs and managers can streamline VA buyer screening and maintain compliance with TenantEvaluation’s QuickApprove platform.

Step-by-Step Guide to the VA Approved Condo Lookup Tool

The official VA Condo Report database gives the most accurate information about condo approval status and helps you avoid bad data from unverified lists or MLS descriptions. Use this tool as your single source of truth when you evaluate Florida condos for VA financing.

Follow these steps to search for VA-approved condos in Florida:

Step 1: Go to the official VA Condo Report at https://lgy.va.gov/lgyhub/condo-report.

Step 2: Select “Florida” from the state dropdown menu.

Step 3: Enter your target city if you want local results, or leave this field blank to see statewide options.

Step 4: Type the condo development name, or use a partial name, or enter the 6-character Condo ID if you already have it.

Step 5: Filter for “approved-only projects” so you focus on developments that already qualify.

Step 6: Review the approval status closely and look for “Accepted Without Conditions” or “Accepted With Conditions.”

Step 7: Check the status again during escrow because VA approval status can change and should be confirmed before ordering appraisals.

Approval status labels carry real consequences for buyers. “Accepted Without Conditions” means the condo is fully approved and you can move forward much like a single-family home purchase. “Accepted With Conditions” means the VA requires extra documentation that acknowledges specific issues. “Unaccepted” means the development is not eligible for VA financing.

MLS listings often show incorrect or outdated VA status, which creates a common verification trap for buyers and agents. You should always confirm status in the official VA database using the exact project name and correct location so you do not waste time on ineligible properties.

Florida HOAs face growing workloads as more VA buyers request confirmation of condo eligibility. TenantEvaluation helps boards and managers handle this demand with automated purchaser screening, custom rules, and community analytics, which can reduce approval times by up to 70 percent and generate revenue through fee sharing. See how TenantEvaluation streamlines VA buyer verification.

How Florida Cities Affect VA Condo Approval Results

Once you know how to search the VA database, city-specific patterns help you interpret the results and choose stronger communities. Local insurance costs, investor activity, and rental rules often explain why some projects appear as approved while similar ones do not.

Miami-Dade County: High-rise condos in Miami, Fort Lauderdale, and Palm Beach receive extra scrutiny because of insurance volatility and coastal risk. South Florida condos frequently require full lender review due to coastal exposure, rising insurance costs, and aging buildings. Many developments also struggle with investor concentration limits and strict rental restrictions, which often show up as conditions or denials in the VA report.

Tampa Bay Area: Tampa, St. Petersburg, Clearwater, and Sarasota usually offer more VA-approved options, especially in newer communities with higher owner-occupancy. However, high investor concentration and low owner-occupancy ratios increase default risk during economic slowdowns, and these factors can push some projects out of VA eligibility.

Central Florida: Orlando and nearby cities provide a wide mix of housing, yet tourist-heavy zones often rely on short-term rentals. Those rental patterns can conflict with VA leasing rules and affect whether a condo appears as approved, conditional, or unaccepted in the database.

Southwest Florida: Fort Myers and Naples have seen more VA approvals in recent years, especially in developments with strong reserves and consistent HOA financial practices. These traits usually support stable insurance coverage and cleaner VA reviews.

Northeast Florida: Jacksonville offers many VA-approved options, particularly in military-friendly communities near naval bases. These projects often design their rules with VA and other government-backed loans in mind.

Several statewide trends now shape VA condo approvals in 2026. Insurance premiums continue to rise, HOA reserve requirements have tightened, and about 10 percent of condos fail VA approval because of unacceptable HOA leasing rules. Veterans get better results when they focus on developments with clear rental allowances, stable insurance coverage, and transparent financials.

Community Association Managers who juggle multiple VA buyer files can simplify their workload with TenantEvaluation’s QuickApprove dashboard. The platform supports real-time VA buyer reviews, board voting, and complete audit trails, and it is built for Florida associations with direct TransUnion and Equifax reseller access. Discover how QuickApprove supports faster, compliant VA decisions.

How Hard Is It to Get a Condo VA Approved in Florida?

Common Reasons Florida Condos Do Not Accept VA Loans

Many Florida condos do not qualify for VA approval because their governing documents conflict with VA leasing rules. The VA requires that HOAs allow leasing, prohibit “seasoning clauses” that force owners to occupy before leasing, and prevent boards from approving or denying individual leases or imposing tenant background or credit checks. Florida HOAs often use these exact tools to control renters, which automatically disqualifies them from VA approval.

Other factors can also block approval. Owner-occupancy rates below 50 percent, more than 25 percent of owners delinquent on HOA dues, or a single entity owning more than 10 percent of units all raise risk for the VA. South Florida HOAs also tend to enforce rental rules such as six- or twelve-month minimum lease terms, waiting periods before new owners can rent, and limits on the number of leases per year, which often conflict with VA standards.

VA Approved Condo Lookup by Address and Ongoing Verification

Knowledge of these disqualifying factors makes your verification process more targeted and efficient. You can review the VA database with a clear sense of which rules might cause problems and which communities are more likely to keep their approval over time.

Use this checklist when you verify a specific condo’s status and monitor it through escrow:

• Search the official VA database using the exact development name.

• Confirm that the address matches exactly, because buildings within the same complex can carry different approval statuses.

• Review any conditions attached to the approval and discuss them with your lender.

• Check that the approval has not been withdrawn or expired as your closing date approaches.

• Ask your lender to confirm current status again during underwriting.

Many buyers assume a condo is VA eligible without checking, yet approval for an unapproved complex can take months. That delay can derail a purchase if you discover the issue too late.

Unapproved condos require a long and document-heavy review. The VA review process typically takes two to three months or longer and depends on HOA cooperation to supply covenants, bylaws, budgets, plat maps, special assessment details, litigation statements, and recent meeting minutes. If the HOA refuses to cooperate, the approval process usually stops completely.

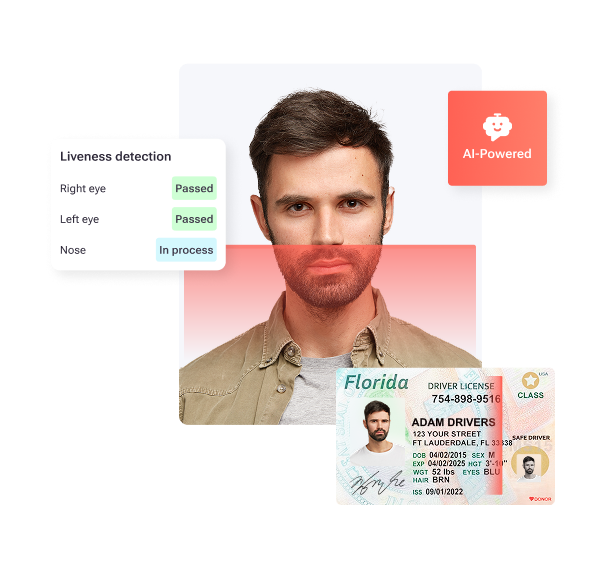

Florida HOAs can reduce fraud risk during this process with TenantEvaluation’s IDVerify+ biometric verification. This feature sits inside the screening workflow and provides seamless KYC checks without redirects, which works well for high-stakes VA purchasers. Learn more about IDVerify+ biometric verification.

Conclusion and Practical Next Steps

Successful VA condo purchases in Florida depend on early verification in the official VA database, awareness of local market challenges, and realistic expectations about timing. Veterans should confirm approval status before making offers, keep backup properties in mind, and partner with experienced VA lenders who understand Florida’s condo rules and insurance climate.

Florida HOAs and Community Association Managers can protect their communities and create new revenue streams by modernizing how they review VA buyers. TenantEvaluation supports more than 5,000 communities, processes over 100,000 applications each year, and saves clients up to 50 hours per day through automated workflows. Leading management companies such as RealManage and Castle Group rely on this platform.

TenantEvaluation began in Florida and built its system around compliant resident screening with FCRA standards at the core. Communities can reduce risk, generate screening revenue, and approve qualified VA buyers with far less manual work. Get started with TenantEvaluation.

Frequently Asked Questions

How can I tell if a condo is VA approved?

Use the official VA Condo Report and search by state and development name. Look for “Accepted Without Conditions” or “Accepted With Conditions” status. Avoid relying on MLS listings or verbal assurances, because those sources often contain outdated or incorrect information.

Is there a VA approved condo list for Florida in PDF format?

The VA does not publish downloadable PDF lists. The online database updates in real time and gives the most accurate approval statuses. You can create custom reports by city or region in the tool, but always confirm status again during your purchase because approvals can change.

Why are not more Florida condos VA approved?

Florida faces unique obstacles such as strict HOA rental restrictions, high investor concentrations, insurance volatility from coastal exposure, and aging buildings that require strong reserves. Many HOAs also use right-of-first-refusal clauses, rental waiting periods, or tenant screening rules that conflict with VA standards and block approval.

Can I use a VA loan on a condo that is “under review”?

You cannot close with a VA loan until the condo receives an official approval status. Lenders are not allowed to order appraisals for unapproved developments. If you pursue a property that is under review, plan for at least a two to three month wait and keep backup options ready because approval is not guaranteed.

How does TenantEvaluation help HOAs with VA buyers?

TenantEvaluation offers an all-in-one platform built for Florida community associations that need to screen VA buyers quickly and compliantly. The QuickApprove dashboard gives boards real-time visibility into applications and supports structured voting, while IDVerify+ biometric verification helps prevent fraud.

The platform can reduce approval times by up to 70 percent and generate revenue through fee sharing, which makes it a strong fit for HOAs that manage frequent VA buyer applications.