Last updated: March 1, 2026

Key Takeaways

- Florida HOA fraud has surged over 30% in 2026, so boards must follow House Bill 1203 and Chapter 720 amendments to protect association funds.

- BankUnited tools such as Payee Positive Pay, ACH alerts, dual signatures, and segregated duties create strong banking controls against check and electronic fraud.

- Annual independent audits, seven-year record retention, and D&O insurance with cyber coverage support regulatory compliance and reduce financial risk.

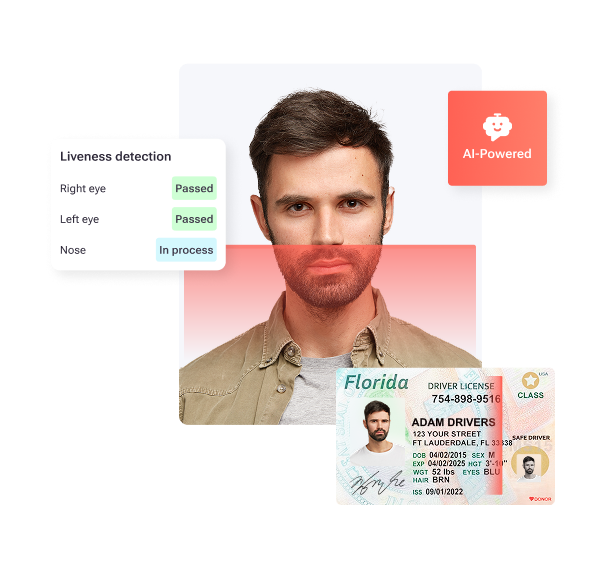

- Biometric ID verification with IDVerify blocks identity fraud during resident onboarding by using liveness detection and facial matching instead of relying only on documents.

- Associations that follow these 10 steps with Tenant Evaluation gain comprehensive FCRA-compliant screening and stronger fraud protection.

Step 1: Use Payee Positive Pay and ACH Alerts with BankUnited

BankUnited Payee Positive Pay requires pre-authorization of every check recipient and amount before processing. Upload an approved payee list to the banking platform so any checks written to unauthorized vendors are automatically flagged for review. This control stops fraudulent checks from clearing your association accounts.

ACH alerts send real-time notifications for electronic debits and credits. Configure alerts for transactions above thresholds that match your association’s normal expenses. Choose banks that provide Positive Pay, multi-factor authentication, and clear protocols for suspicious activity to create a complete fraud defense.

Implementation Checklist:

- Enable Payee Positive Pay for every checking account

- Set ACH alerts for transactions over $500

- Review and approve payee lists each month

- Designate two board members to receive alert notifications

Step 2: Require Dual Signatures and Multi-Factor Authentication

Florida HOAs should require dual signatures from board members for all checks above a set amount, often $1,000 or the level in the governing documents. This structure prevents any single person from authorizing large expenditures alone.

Multi-factor authentication, or MFA, adds a second layer of security to online banking access. Require password updates every 90 days and use token-based or SMS verification for all banking logins to reduce account takeover risk.

Implementation Checklist:

- Set dual signature rules for checks over $1,000

- Enable MFA on all banking platform accounts

- Rotate banking passwords every quarter

- Limit banking access to authorized board members only

Step 3: Separate Financial Duties Inside the HOA

Segregation of duties keeps one person from controlling recording, authorizing, and reconciling financial transactions. The person who writes checks should not reconcile bank statements or maintain accounting records.

Florida associations should assign different people to check preparation, approval, and account reconciliation. This structure creates several review points for each transaction and reduces opportunities for internal fraud.

Implementation Checklist:

- Assign check writing to one board member

- Designate a different member for check approval

- Use a third party to handle bank reconciliation

- Rotate financial responsibilities each year

Step 4: Meet 2026 Florida HOA Audit and Record Rules

House Bill 1203 sets operational baselines for HOAs in 2026 and allows severe penalties, including criminal charges, for non-compliant board members. Independent annual audits are mandatory for associations that meet specific thresholds.

Official records must stay on file for at least seven years unless governing documents require a longer period. This retention window supports complete audit trails and detailed fraud investigations.

2026 Compliance Checklist:

- Schedule annual independent audits

- Maintain financial records for at least seven years

- Confirm website compliance for associations with 100 or more parcels

- Document all board financial decisions in meeting minutes

Step 5: Control Vendor Payments and Eliminate Cash

Boards should verify every vendor invoice against approved contracts and purchase orders before payment. Fraudulent vendors often send inflated or duplicate invoices to associations that skip this verification step.

Eliminate cash transactions from association operations. Route all payments through traceable banking channels with clear documentation. This policy prevents off-the-books spending and supports full financial transparency.

Implementation Checklist:

- Require purchase orders for all vendor services

- Match invoices to contracts before issuing payment

- Prohibit cash transactions across the association

- Maintain vendor payment logs with approval signatures

Step 6: Screen Managers and Strengthen Insurance Coverage

Boards should run comprehensive background checks on all property managers and financial staff who can access association funds. Screening should include criminal history, credit checks, and verification of professional licenses and certifications.

Directors and Officers, or D&O, insurance protects against theft, forgery, and financial mismanagement claims. Confirm that policies include coverage for employee dishonesty and cyber fraud aimed at association accounts.

Implementation Checklist:

- Background check all financial personnel each year

- Verify professional licenses and certifications regularly

- Maintain adequate D&O insurance limits

- Add cyber fraud protection to insurance policies

Step 7: Train the Board and Secure Association Technology

Ongoing board education through Florida Community Association Institute (FCAP) and FirstService training keeps members aware of new fraud schemes and prevention tactics. Associations also need legal counsel to confirm that board actions are authorized and reasonable, which reduces liability during fraud prevention efforts.

Associations should enable multi-factor authentication across all technology platforms, including property management software, email, and financial applications. Secure systems reduce unauthorized access to sensitive association data.

Implementation Checklist:

- Attend quarterly FCAP fraud prevention seminars

- Enable MFA on every association technology platform

- Update software and security patches each month

- Train board members to recognize phishing and social engineering

Four Core Pillars of HOA Fraud Prevention

Effective HOA fraud prevention rests on four connected pillars that combine BankUnited banking tools with modern resident verification.

- Segregated Financial Controls: Dual signatures, separated duties, and independent reconciliation reduce internal fraud risk.

- Independent Audits and Compliance: Annual audits, seven-year record retention, and regulatory compliance create transparency.

- Secure Technology Infrastructure: MFA, encrypted platforms, and regular security updates protect digital assets.

- Biometric Resident Screening: Identity verification with TenantEvaluation’s IDVerify blocks fraudulent occupants.

Florida HOA Fraud Prevention Strategy Overview

Florida HOA fraud prevention strategies combine traditional banking controls with modern identity verification technology.

- Banking Layer: BankUnited Positive Pay, ACH alerts, dual signatures, and segregated duties.

- Audit Layer: Independent annual audits, extended record retention, and compliance monitoring.

- Technology Layer: Multi-factor authentication, secure platforms, and encrypted communications.

- Identity Layer: Biometric verification, government ID validation, and liveness detection during resident onboarding.

Step 8: Add Biometric ID Verification to Screening

Traditional resident screening relies on uploaded documents and cannot reliably stop identity theft, impersonation, or synthetic identity fraud. IDVerify adds biometric identity checks to the screening workflow by using government ID validation, AI-powered liveness detection, and facial matching to confirm that applicants are real, present, and matched to their identification.

This TenantEvaluation solution runs natively inside the platform without third-party redirects, which strengthens fraud prevention for community associations while keeping the applicant experience smooth. It also aligns with PCI Level 1 compliance and end-to-end encryption.

Schedule a demo today to see how biometric verification keeps fraudulent residents out of your community.

Step 9: Use TenantEvaluation for FCRA-Compliant Screening

TenantEvaluation’s QuickApprove dashboard gives boards direct access to application status, summary reports for each applicant, and a voting panel for approvals. These reports include background checks, income verification, and biometric identity confirmation.

FCRA compliance serves as the foundation of the platform through direct credit bureau reseller relationships, automated adverse action workflows, and built-in audit trails for every application. TenantEvaluation processes more than 100,000 applications each year and holds a 4.8 out of 5 Google rating, with a focus on community associations rather than generic rental properties.

Step 10: Compare TenantEvaluation with ApplyCheck and Verify Screening

| Feature | TenantEvaluation | ApplyCheck | Verify Screening |

|---|---|---|---|

| Biometric Verification | Yes (IDVerify+) | No | No |

| End-to-End Automation | Complete Platform | Partial | Partial |

| Time Savings | Up to 70% | Unknown | Unknown |

| Revenue Model | Revenue Sharing | Subscription | Subscription |

TenantEvaluation’s integrated model combines BankUnited-compatible financial controls with advanced biometric screening technology, which delivers a level of fraud prevention that competing platforms do not provide.

Frequently Asked Questions

How does BankUnited Positive Pay prevent HOA fraud?

BankUnited Positive Pay requires pre-authorization of all check recipients and amounts before processing. Associations upload approved payee lists to the banking platform, and any unauthorized checks are automatically flagged for review. This process keeps fraudulent checks from clearing association accounts and offers real-time protection against check fraud schemes that target HOA finances.

What is the best biometric screening solution for Florida HOAs?

TenantEvaluation’s IDVerify provides comprehensive biometric identity verification built for Florida community associations. The system uses government ID validation, AI-powered liveness detection, facial landmark recognition, and biometric selfie-to-ID comparison to stop identity fraud during resident onboarding. IDVerify runs natively within the TenantEvaluation screening workflow without external redirects and maintains FCRA compliance and PCI Level 1 security standards.

How does TenantEvaluation compare to Snappt for fraud prevention?

Snappt focuses mainly on income verification, while TenantEvaluation delivers end-to-end fraud prevention through biometric identity verification, full background screening, and FCRA-compliant workflows. TenantEvaluation’s IDVerify+ prevents identity theft and impersonation attempts that document-only systems miss, and the QuickApprove dashboard gives boards direct oversight of the entire screening process. The revenue-sharing model also generates income for associations instead of requiring subscription fees.

What are the 2026 Florida HOA audit requirements?

Florida HOAs must conduct annual independent audits under House Bill 1203, maintain financial records for at least seven years, and ensure website compliance for associations with 100 or more parcels. These rules create operational baselines and allow severe penalties, including criminal charges, for board members who ignore them. The longer record retention period supports complete audit trails that are essential for fraud investigation and prevention.

Why is segregation of duties critical for HOA fraud prevention?

Segregation of duties keeps any single individual from controlling recording, authorizing, and reconciling financial transactions. Florida associations should assign separate roles for check preparation, approval, and account reconciliation to reduce internal fraud. This basic control creates multiple oversight points for all financial activities and makes fraudulent transactions require collusion between several people, which significantly lowers fraud risk.

Florida HOA fraud prevention works best when boards combine BankUnited banking tools with advanced biometric screening technology. These 10 steps create a strong foundation for fraud protection, and success depends on choosing the right technology partners. Schedule a demo today to start protecting your association with integrated BankUnited and TenantEvaluation fraud prevention solutions.