Key Takeaways for Florida Condo Buyer Screening

- Financially unstable condo buyers increase the risk of HOA defaults, special assessments, and declining property values for Florida communities.

- Use a 7-step checklist that covers income verification, DTI ratios under 36%, credit scores above 680, and 3 to 6 months of reserves.

- Watch for red flags such as DTI over 50%, recent bankruptcies, employment gaps, and identity fraud patterns.

- Maintain FCRA compliance with clear disclosures, written authorizations, and proper adverse action notices during screening.

- Automate screening with TenantEvaluation to cut processing time by 70% and strengthen fraud prevention for your community.

Why Financial Stability Matters for Florida Condo Buyers

Financially unstable buyers create cascading risks for condo associations. Missed HOA payments can trigger special assessments and even foreclosure proceedings that reduce property values across the community. Lenders now view debt-to-income ratios near or above 50% as higher risk, yet many associations still lack systematic processes to verify these critical financial metrics before approval.

The 2026 landscape presents additional challenges with property records showing increased patterns of frequent ownership turnover, outstanding liens, and foreclosure histories that signal potential buyer instability. Given these elevated risks, CAMs and boards have heightened fiduciary duties to make informed approval decisions that protect association finances and comply with Fair Credit Reporting Act requirements. See how TenantEvaluation’s community analytics reveal buyer trends across your portfolio.

7-Step Checklist to Assess Condo Buyer Financial Stability

This 7-step checklist gives CAMs and boards a clear, repeatable process to evaluate prospective condo buyers while staying compliant and efficient.

Step 1: Verify Income Beyond Self-Reporting

Request recent pay stubs, tax returns, and employment verification letters directly from employers, because self-reported income figures are insufficient for accurate assessment. TenantEvaluation’s IncomeEv solution automates this verification process by contacting employers directly and generating comprehensive income verification reports that eliminate guesswork.

Step 2: Calculate Debt-to-Income Ratios

Most lenders follow the 28/36 rule, preferring front-end DTI at or below 28% and back-end DTI at or below 36%, though 43% remains widely accepted. For condo buyers, ideal DTI should remain under 36% to account for HOA fees and potential special assessments. The following table shows how different DTI ranges translate into risk levels and approval recommendations.

| DTI Range | Risk Level | Recommendation |

|---|---|---|

| Under 36% | Low Risk | Approve with standard review |

| 36-43% | Moderate Risk | Require additional reserves |

| Above 50% | High Risk | Reject or require significant compensating factors |

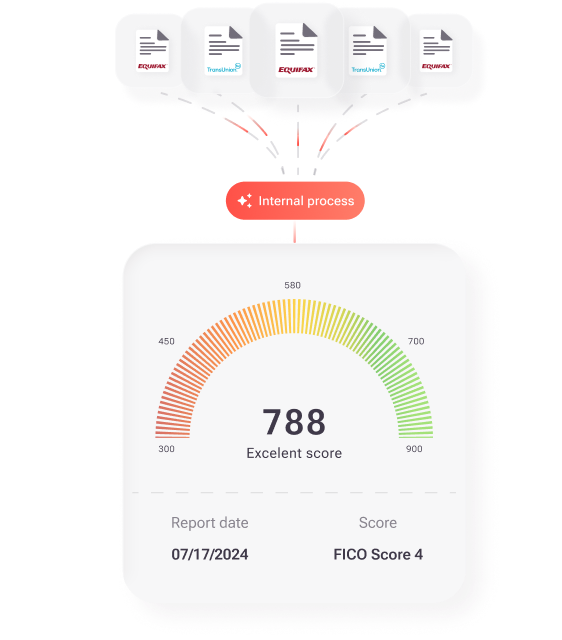

Step 3: Review Credit History and Scores

Obtain FCRA-compliant credit reports and look for scores above 680 for stronger approval confidence. Review payment history, outstanding debts, and recent credit inquiries in detail. TenantEvaluation’s SafeCheck+ solution provides comprehensive background screening with built-in FCRA compliance and complete audit trails.

Step 4: Assess Liquid Assets and Reserves

Fannie Mae requires 0 to 12 months minimum reserves depending on loan type and DTI ratios. For condo buyers, require 3 to 6 months of housing payments in liquid reserves to cover potential special assessments and maintenance fee increases without stressing monthly cash flow.

Step 5: Confirm Employment Stability

Verify at least 2 years of consistent employment history in the same field or with the same employer. Recent job changes or gaps in employment history can indicate income instability that may affect long-term payment ability and association cash flow.

Step 6: Identify Financial Red Flags

Watch for warning signs including DTI ratios exceeding 50%, recent bankruptcy filings, multiple late payments, inconsistencies between reported and verified income, or patterns of frequent property ownership turnover or outstanding liens in previous property records. Treat clusters of these issues as indicators of higher risk that warrant closer review or denial.

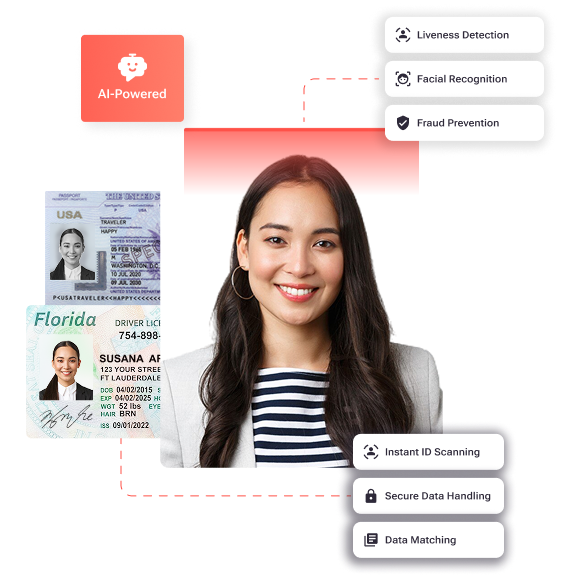

Step 7: Implement Biometric Identity Verification

Strengthen fraud prevention with liveness detection and biometric facial matching to confirm applicant identity. TenantEvaluation’s IDVerify solution validates government-issued IDs and uses AI-powered biometric comparison to eliminate synthetic identity fraud and impersonation attempts. The table below compares manual screening with the TenantEvaluation platform across key operational metrics.

| Process Aspect | Manual Method | TenantEvaluation Platform |

|---|---|---|

| Processing Time | 3-5 days | 4-6 hours (70% faster) |

| FCRA Compliance | Manual tracking, high risk | Automated workflows, built-in compliance |

| Fraud Detection | Document review only | Biometric IDVerify verification |

| Board Access | Email attachments | QuickApprove dashboard with voting panel |

TenantEvaluation’s integrated platform serves over 5,000 communities, processing about 100,000 applications annually while generating $150 million in revenue for communities. As a direct TransUnion and Equifax reseller, the platform delivers data accuracy and compliance that manual processes cannot match. Discover how automation can reduce your screening workload and increase association revenue.

Financial Red Flags and Common Screening Pitfalls

Several recurring warning signs point to potential buyer financial instability and deserve immediate attention from boards and CAMs.

- Unverified or inconsistent income documentation between pay stubs, tax returns, and employer verification

- Poor liquidity with insufficient reserves to cover 3 to 6 months of housing expenses

- Mismatched identification documents or suspicious property ownership patterns that suggest identity fraud

- Recent bankruptcy, foreclosure, or multiple late payments within the past 24 months

- Employment gaps or frequent job changes indicating income instability

Best practices focus on using automated verification tools to reduce human error and apply consistent evaluation standards across all applicants. TenantEvaluation’s multi-layer fraud prevention system combines income verification, credit screening, and biometric identity confirmation to deliver a comprehensive buyer assessment. Explore IDVerify+ and see how it closes identity fraud gaps in your current process.

FCRA Compliance for Florida Condo Buyer Screening

The Fair Credit Reporting Act requires clear written disclosure before obtaining consumer reports, prior written consumer authorization, and adverse action notices when rejecting applications based on credit information. Florida condo associations must establish permissible purpose for accessing credit reports and maintain proper documentation throughout the screening process.

TenantEvaluation operates as a direct credit bureau reseller with built-in FCRA compliance, automated adverse action workflows, and complete audit trails for every application. The platform separates decision-making authority, which remains with the association, from data provision, which TenantEvaluation handles, to maintain a compliant structure. Request a compliance review to identify gaps in your current FCRA procedures.

Conclusion: Build a Reliable Condo Buyer Screening Framework

Systematic assessment of condo buyer financial stability protects associations from defaults, special assessments, and legal liability while supporting long-term community financial health. This 7-step checklist provides a practical framework for thorough evaluation, yet manual processes struggle to scale and maintain consistent compliance standards.

TenantEvaluation’s specialized platform automates the entire buyer screening workflow with FCRA compliance as the foundation. With a 4.8 out of 5 Google rating and proven results at scale, the platform streamlines operations while generating revenue through its pay-per-application model. Connect with Florida’s most trusted condo buyer screening partner to modernize your approval workflow.

FAQ

What DTI ratio should condo buyers maintain?

Ideal debt-to-income ratios for condo buyers should remain under 36% to account for HOA fees and potential special assessments. Conventional mortgages may approve up to 43 to 45% DTI, yet condo associations should apply stricter standards because of the additional financial obligations of community living. Ratios exceeding 50% represent significant risk and typically warrant rejection unless substantial compensating factors exist.

What are the biggest red flags indicating financial instability in condo buyers?

Major warning signs include DTI ratios above 50%, recent bankruptcy or foreclosure within 24 months, unverified or inconsistent income documentation, and insufficient liquid reserves below 3 months of housing expenses. Frequent job changes, employment gaps, patterns of late payments, and outstanding liens also raise concern. Identity fraud indicators such as mismatched documentation or suspicious property ownership history signal high risk and require deeper investigation.

Is conducting credit checks on condo buyers legally required?

Credit checks are not legally mandated, yet they provide essential information for informed approval decisions and help associations fulfill their fiduciary duties. When conducting credit screening, associations must comply with FCRA requirements including proper disclosure, written authorization, and adverse action notices. Credit scores above 680 are generally preferred, while scores below 620 indicate higher risk and may require stronger compensating factors.

How does biometric verification help prevent condo buyer fraud?

Biometric identity verification uses AI-powered liveness detection and facial recognition to confirm that applicants are real people physically present during the application process. This approach blocks synthetic identities and impersonators who rely on stolen documents. The technology validates government-issued IDs and compares facial biometrics to detect identity fraud that traditional document-based screening often misses.

Why choose TenantEvaluation over other screening providers?

TenantEvaluation focuses exclusively on Florida community associations and management companies and delivers features many competitors lack, including the QuickApprove board dashboard, integrated biometric verification, a revenue-sharing model, and FCRA compliance as a core design principle. As a direct credit bureau reseller serving 5,000+ communities, TenantEvaluation provides comprehensive automation that reduces processing time by up to 70% while generating revenue for associations.