Written by: Luis Teran, Co-founder, CEO, TenantEvaluation

Key Takeaways

- Stronger credit and criminal screening helps Florida HOAs and condos manage rising costs, support SIRS funding, and protect community stability.

- Clear, consistent criteria and documented processes reduce Fair Housing and FCRA risk while improving transparency for applicants and owners.

- Recent Florida laws on reserves, transparency, and anti-fraud initiatives increase the need for reliable financial and background checks.

- Modern digital platforms cut administrative work, improve data security, and give boards better visibility into each application.

- TenantEvaluation provides Florida-focused, compliant screening with automated workflows, secure data handling, and an easy onboarding process for associations and applicants. Schedule a demo to see how it works.

Understanding Credit and Criminal Screening Services in HOA/Condo Management

How Credit Screening Supports Financial Stability

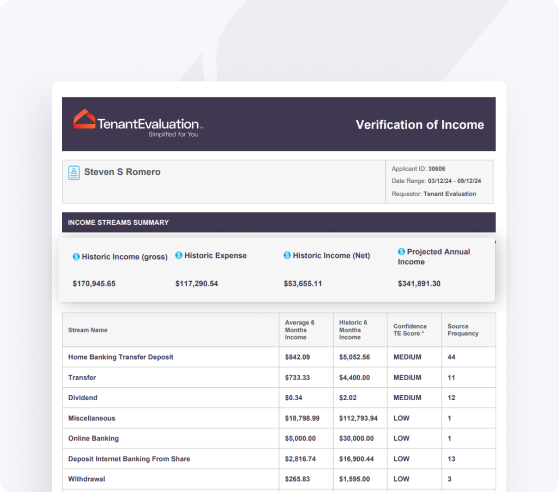

Credit screening evaluates an applicant’s financial history and behavior through authorized credit reports. Key metrics include payment history, outstanding debts, credit utilization, and overall financial behavior to assess financial stability and potential for timely fee payments. For HOAs and condominiums, this review helps predict whether prospective residents can reliably pay monthly assessments, special assessments, and future increases tied to new state regulations.

Effective credit review focuses on patterns of on-time housing payments, realistic debt-to-income ratios, responsible use of available credit, and an overall score that signals reliability. These factors matter more as communities plan for long-term structural work and rising operating costs.

How Criminal Screening Protects Community Safety

Criminal background screening examines nationwide criminal records, sex offender registries, and applicable watchlists to identify safety risks. Only specific convictions relevant to safety and property value, such as violent crimes, sex offenses, and financial crimes, are commonly evaluated, since broad bans or inconsistent decisions increase legal risk.

A focused approach considers the nature of the offense, its recency, and any demonstrated risk to residents or property. Consistent standards, applied uniformly, help avoid Fair Housing issues while supporting a safe environment.

Complying with FCRA and Florida Fair Housing Requirements

Compliance with the Fair Credit Reporting Act (FCRA), federal Fair Housing Act, and Florida Fair Housing Act is essential. Florida associations must follow discrimination prohibitions, obtain written consent, and provide required disclosures when using credit and criminal reports.

The FCRA requires written consent before screening, clear disclosure of criteria, and proper adverse action notices when denying based on report findings. Fair Housing laws require neutral, objective standards that do not target protected classes.

Florida’s Unique Landscape: 2025 Trends and Legislative Impacts on Screening

New Laws Raising Financial and Governance Standards

Chapter 2025-16, L.O.F. (2025), increases structural, financial, reporting, and education requirements for Florida associations, including stricter Structural Integrity Reserve Studies (SIRS) for buildings three or more habitable stories. At the same time, new and proposed legislation targets abusive practices, strengthens financial oversight, and adds state-level fraud investigation and database transparency measures.

SIRS and Higher Financial Expectations for Owners

SIRS requirements obligate qualifying condominiums to complete structural assessments and fund reserves for major repairs under detailed documentation rules. These changing funding rules make accurate, current financial data during screening essential, since new residents must support increased assessments and reserve contributions.

Transparency, Documentation, and Screening

Legislative focus on transparency and fairness points toward stronger documentation and consistent application of screening policies. Associations benefit from clear records of criteria, decisions, and notices to align with these expectations.

Integrating Credit and Criminal Screening Services into Your HOA/Condo Operations

Confirming Screening Authority in Governing Documents

Authority to screen buyers or tenants must appear in governing documents to be enforceable, especially for criminal history checks. Boards should work with association counsel to confirm that declarations, bylaws, and rules clearly authorize:

- Credit and criminal background checks

- Collection of application and screening fees

- Objective approval and denial criteria

Creating Consistent, Objective Screening Criteria

Clear criteria reduce disputes and legal exposure. Best practices include written standards, transparent fee schedules, documented decisions, and automated accounting where possible. Well-designed criteria often define:

- Minimum acceptable credit scores and income levels

- Debt-to-income thresholds that account for fees and likely assessments

- Types of criminal convictions that may lead to denial, with guidance on recency and severity

Protecting Applicant Data and Privacy

Secure handling of personal data is essential to limit liability. Inadequate privacy practices can lead to fines and lawsuits, so associations need clear rules for storage, access, retention, and disposal of sensitive records.

Strong programs restrict access to authorized users, encrypt stored information, and follow defined timelines for secure destruction of records that are no longer required.

TenantEvaluation provides a controlled, encrypted environment that helps boards manage this data responsibly. Request a demo to review the workflow.

Common Challenges and Pitfalls in HOA/Condo Screening

Legal Risk from Inconsistent Processes

Uneven application of standards or failure to follow FCRA steps can result in discrimination claims or regulatory action. Frequent issues include missing written consent, inconsistent treatment of similar criminal records, and informal decision-making without documentation.

Board members and staff benefit from brief, recurring training on Fair Housing rules and standard operating procedures for each application.

Heavy Administrative Workloads

Paper-based applications and manual coordination consume time and create delays for buyers, tenants, and real estate agents. Staff need to chase documents, verify information, coordinate with multiple vendors, and maintain records for potential audits.

Digital tools reduce repetitive tasks, centralize records, and shorten approval timelines.

Data Security and Communication Gaps

Handling Social Security numbers and financial records through email or paper files raises breach risk and complicates compliance. Poor communication about requirements and timelines often results in incomplete applications and avoidable denials. Clear, published screening criteria and process overviews help reduce misunderstandings and disputes.

Best Practices and Emerging Standards for Compliant Screening in 2025

Using Automated and Integrated Screening Platforms

Modern associations increasingly rely on secure online platforms for application intake, document collection, background checks, and approvals. These systems:

- Lower administrative burden and manual data entry

- Reduce risk of lost or incomplete files

- Create standardized, repeatable workflows

Aligning Workflows with Florida Regulations

Systems built with Florida associations in mind can reflect SIRS timelines, local disclosure rules, and typical governing document clauses. Customizable workflows let boards align platform settings with their own policies and community standards while preserving compliance with state and federal law.

Enhancing Security for Sensitive Information

Advanced screening platforms offer bank-level protections, including PCI Level 1 compliance, encryption, and automatic redaction of sensitive data. These features limit exposure while allowing boards to review the information needed for sound decisions.

Improving Board Visibility and Audit Trails

Dedicated board portals provide real-time status tracking, structured voting, and automatic logs of every action on an application. These audit trails support transparency, simplify responses to owner questions, and document compliance efforts for regulators or legal counsel.

TenantEvaluation incorporates these practices into a single platform tailored to HOA and condo screening. Get started to modernize your process.

Comparing Screening Solutions: TenantEvaluation vs. Traditional Methods

|

Feature |

TenantEvaluation |

Manual Processes |

Generic Providers |

|

Compliance (FCRA/Fair Housing) |

Automated, documented workflows |

Manual, error-prone steps |

Limited policy customization |

|

Efficiency and Automation |

Digital forms, automated checks, redaction |

Paperwork, email chains, manual follow-up |

Partial automation only |

|

Data Security |

PCI Level 1, encryption, controlled access |

Variable safeguards, higher breach risk |

Basic security tools |

|

Board Transparency |

Board dashboards, voting tools, audit logs |

Scattered emails and files |

Few board-focused features |

Frequently Asked Questions (FAQ)

Which criminal offenses can a Florida HOA consider during screening?

Florida associations generally focus on convictions that relate directly to safety and property value, such as violent crimes, certain sex offenses, major property crimes, and serious financial fraud. Decisions should weigh the type of offense, how long ago it occurred, and any ongoing risk. Governing documents need to authorize criminal checks, and policies should avoid blanket bans that may conflict with Fair Housing guidance.

How do recent Florida financial transparency laws affect screening?

New laws increase reserve and reporting requirements, especially for buildings covered by SIRS. These changes can result in higher assessments or new funding obligations, which makes careful review of income, debt, and payment history more important. Consistent standards help ensure that new residents can meet both current and foreseeable financial commitments.

Is it permissible for an HOA to charge application fees for background checks?

Reasonable application fees are generally allowed in Florida when used to cover legitimate screening costs. Fees should be disclosed in advance, applied evenly to all similar applicants, and supported by governing document language that authorizes their collection. Excessive or inconsistent fees can invite complaints or legal challenges.

Conclusion: Building Secure, Compliant Communities Through Smart Screening

Well-structured credit and criminal screening programs help Florida HOA and condo communities manage regulatory change, protect residents, and stabilize finances. Robust, compliant screening can also support association income, community reputation, and long-term satisfaction while limiting legal exposure.

TenantEvaluation supports these goals with Florida-aware workflows, strong data security, and tools designed for boards and managers. Schedule a demo today to streamline your credit and criminal screening process.