Written by: Luis Teran, Co-founder, CEO, TenantEvaluation

Key Takeaways for Florida Condo Approvals

- Florida condo and HOA boards must follow statutory requirements under Sections 718.112 and 718.503 when screening buyers and renters, including specific document packages, fee caps, and timelines that generic tools do not address.

- A 10-step approval checklist covers everything from confirming governing document authority and collecting required documents to running FCRA-compliant background checks and issuing proper notices.

- Common red flags such as incomplete submissions, identity inconsistencies, low reserve funding, and modern fraud tactics like deepfakes can delay approvals or trigger rejections if boards do not catch them early.

- Biometric identity verification and automated workflows reduce fraud risk and speed up board review while maintaining full compliance and audit trails.

- Get started with TenantEvaluation to automate Florida-specific condo board approvals inside one FCRA-compliant platform.

10-Step Condo Board Approval Checklist

- Confirm governing document authority. Verify that the declaration, bylaws, and rules authorize the association to screen and approve the applicant type, whether buyer or renter.

- Distribute the correct application package. Provide applicants with a community-specific form that separates buyer and renter workflows and captures all required fields.

- Collect required documents. Gather government-issued photo ID, executed lease or purchase contract, proof of income or financials, and any community-specific supplemental forms.

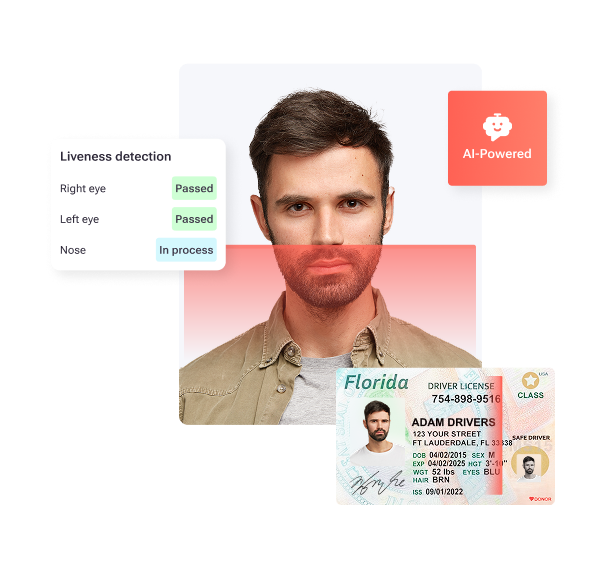

- Verify identity. Confirm the applicant’s identity with a biometric-backed process that validates government ID authenticity and confirms physical presence.

- Collect the application fee. Charge no more than the amount authorized under Section 718.112(2)(k), Florida Statutes, which starts at $150 per applicant but must be adjusted every 5 years for CPI inflation and published by DBPR, for condominiums, and apply the fee only to screening and transfer approval.

- Run FCRA-compliant background and credit screening. Obtain consumer reports only for permissible purposes, certify those purposes to the reporting agency, and retain documentation.

- Review financials and association health documents. For buyers, confirm the association’s reserve funding, budget, and any pending litigation that could affect lender approval.

- Flag red flags and incomplete submissions. Identify missing documents, identity inconsistencies, financial irregularities, or fraud indicators before advancing the application.

- Conduct board review and vote. Present a complete, summarized application package to the board through a structured review process with a documented voting record.

- Issue decision and required notices. Deliver an approval letter or, if adverse action is based on a consumer report, provide all FCRA-required adverse action disclosures to the applicant.

See how TenantEvaluation automates every step of this checklist inside one FCRA-compliant platform.

Florida Document Rules for Buyers and Renters

Florida law sets different document expectations for purchase applicants and rental applicants, so boards must treat these tracks separately.

For buyers, Section 718.503, Florida Statutes entitles the purchaser, at the seller’s expense, to the declaration of condominium, articles of incorporation, bylaws and rules, the most recent year-end financial statement and annual budget, the inspector-prepared milestone inspection report, the most recent structural integrity reserve study (or a written statement that none was completed), and any turnover inspection report performed on or after July 1, 2023. A practical due-diligence package also includes minutes from recent board meetings and a reserve study, which reveal pending repairs, potential lawsuits, and owner complaints not yet reflected in the budget. Under Section 718.503, buyers have a 15-day right to void the contract after execution and receipt of the required documents, and this right cannot be waived.

For renters, the association’s governing documents define what is required because renters are not purchasing an ownership interest. Standard items include a fully executed lease, government-issued photo ID for all adult occupants, proof of income or employment, and any community-specific supplemental forms. Section 718.112(2)(k), Florida Statutes permits the association to collect a security deposit from a prospective tenant, capped at one month’s rent, when the governing documents authorize it, in addition to any deposit held by the unit owner.

Starting August 3, 2026, Fannie Mae and Freddie Mac are eliminating the limited review process for condo sales, which will require full reviews of association finances, insurance, and overall project health. Boards that prepare detailed lender questionnaire responses in advance reduce delays that can affect buyer financing.

Red Flags That Commonly Trigger Rejections

Incomplete submissions are the most common cause of delays and rejections. Missing documents, unsigned forms, or an unexecuted lease force manual follow-up and stall the board review cycle.

Identity inconsistencies now create significant risk. Advanced identity verification systems flag altered or forged government-issued IDs by analyzing security features such as holograms, microprinting, and watermarks. Mismatched names, addresses, or dates of birth across submitted documents are explicitly listed as red flag categories under the FTC Red Flags Rule and should trigger additional review rather than automatic approval.

Financial red flags include reserve funding below acceptable thresholds. Lenders commonly deny financing when reserve funding falls below 10% of annual operating income or when more than 15% of owners are over 60 days delinquent on dues. On the applicant side, large cash payments from unverified sources and a lack of documentation for significant funds warrant enhanced scrutiny.

Fraud indicators now include synthetic identity creation, AI-generated deepfake impersonation, and SIM-swapping, which document-only review processes cannot reliably detect. Applicants who are reluctant to provide basic identity information or whose background checks reveal inconsistencies with initially disclosed information also present clear warning signs.

Board Review Workflow for Consistent Decisions

A consistent board review workflow starts with a complete, verified application package. Boards should not begin formal review of an incomplete submission because partial reviews create audit gaps and inconsistent treatment across applicants.

Each application should be presented to board members in a standardized format that summarizes screening results, identity verification status, financial indicators, and any flagged items so that decisions rely on comparable information across all applicants. This standardization only works when the board can later demonstrate consistent treatment, which requires all review actions, votes, and communications to be timestamped and retained in a centralized audit trail.

Board-enacted rules cannot contradict the declaration or rights reasonably inferred from it, and rental restrictions, occupancy rules, and pet policies originate in the governing documents. Boards should confirm that any rejection rationale is grounded in the governing documents and applied consistently to reduce fair housing exposure.

Stakeholder communication, including status updates to applicants, realtors, and unit owners, should be automated where possible to reduce manual follow-up and maintain transparency throughout the process.

Identity Verification for Fraud Prevention and FCRA

Traditional document-based screening cannot reliably prevent impersonation or synthetic identity fraud. Liveness detection in biometric analysis confirms the user is a live, three-dimensional person present at the moment of verification and blocks presentation attacks that use photos, videos, or deepfakes. Real-time cross-referencing of ID data against credit bureaus and government watchlists further strengthens identity confirmation.

Under FCRA Regulation V, users of consumer reports must maintain documented policies for recognizing and responding to address discrepancy notices from consumer reporting agencies and must form a reasonable belief that the report relates to the correct consumer before relying on it for application decisions. Forming that reasonable belief is difficult when boards rely only on document review because documents can be forged or stolen. Biometric identity verification supports this requirement by confirming identity authenticity before screening authorization occurs and gives boards a defensible basis for believing that the report matches the actual applicant.

TenantEvaluation’s IDVerify embeds automated KYC verification directly into the screening workflow using government ID validation, AI-powered liveness detection, and biometric facial matching. Verification results, including ID authenticity confirmation, liveness status, and biometric match result, appear inside the screening report alongside a redacted ID copy for compliance documentation. IDVerify can be configured per community or portfolio, which supports different risk profiles without a one-size-fits-all approach.

Timeline Expectations for Florida Condo Approvals

Standard condo board approval timelines in Florida typically range from 2 to 8 weeks depending on community complexity, application volume, and board meeting schedules. Standard sales and sublet applications processed through structured platforms can usually be completed within a few weeks, with expedited options available. Manual workflows that rely on email chains, spreadsheets, and physical document review consistently extend this range and create bottlenecks during peak seasons.

Common delay factors include incomplete submissions that require multiple follow-up rounds, board members lacking real-time visibility into application status, and approval letters that require separate manual preparation after a vote is recorded.

TenantEvaluation’s QuickApprove accelerated approval workflow moves applications from submission to decision faster inside one connected platform. It provides real-time application tracking, automated communication support, a board-ready approval process with a dedicated review and voting dashboard, customized approval letters, and a personalized welcome package, all without losing control, compliance, or visibility. QuickApprove is designed for high-volume seasons and communities with complex onboarding requirements and gives CAMs, boards, and property management teams a cleaner path from review to decision.

See how QuickApprove reduces approval delays with real-time tracking built for your community.

How TenantEvaluation Supports Florida Condo Board Approvals

TenantEvaluation is an all-in-one resident screening and onboarding platform built specifically for Florida community associations and management companies, with FCRA compliance as the foundation, not an afterthought. Founded in 2007, the platform has processed more than 100,000 applications annually across over 5,000 communities and carries a 4.8/5 Google rating.

The platform’s core capabilities cover every stage of the approval checklist. Intelligent form logic differentiates buyer and renter workflows automatically. Automated document review rejects incomplete submissions before they reach the board. PCI Level 1 compliance, end-to-end encryption, and automatic redaction of sensitive PII protect both applicants and associations from data exposure. As a direct reseller of TransUnion and Equifax data, not a third-party scraper, TenantEvaluation provides FCRA-compliant background and credit reports with built-in adverse action workflows and full audit trails.

QuickApprove accelerates resident approvals for CAMs, boards, and property management teams inside one connected platform and replaces email chains and spreadsheets with real-time application tracking, reduced manual follow-ups, and a board-ready approval process that is faster, clearer, more consistent, and easier to manage without removing board oversight.

IDVerify moves communities from document-based validation to biometric-confirmed identity verification, which strengthens approval confidence and reduces liability exposure before residents enter the community.

For age-restricted properties, 55+ Communities Verification is a built-in capability that reduces manual work, standardizes application handling, and supports documentation consistency across applicants. Built for Florida condos and HOAs and designed for Community Association Managers, it improves operational efficiency and strengthens internal processes by replacing fragmented emails, PDFs, and follow-ups with a more structured and scalable workflow for 55+ communities.

Frequently Asked Questions

How long does a Florida condo board approval typically take?

Most Florida condo board approvals take between 2 and 8 weeks from the date a complete application is submitted. The actual timeline depends on the community’s governing documents, board meeting schedule, application volume, and whether the submission is complete on first review. Incomplete applications, such as those with missing documents, unsigned forms, or unverified identity, are the most common cause of delays. Platforms like TenantEvaluation that automate document review, provide real-time tracking, and give boards a dedicated review dashboard can significantly reduce this window without removing board oversight.

What are the most common reasons a Florida condo board rejects an application?

Rejections most often result from incomplete or inaccurate document submissions, failure to meet the community’s financial screening criteria such as minimum credit score or income thresholds, identity inconsistencies between submitted documents, and background check findings that conflict with the governing documents’ occupancy standards. Boards may also reject applications when the association’s own financial health, such as low reserve funding or pending litigation, creates lender approval issues for buyers. Any rejection based on a consumer report requires FCRA-compliant adverse action notices to be delivered to the applicant.

Is the approval process different for renters versus buyers in Florida condos?

Yes. Buyers are entitled by statute to a specific package of governing documents, including the declaration, bylaws, financial statements, and structural integrity reserve study, and they have a statutory right to cancel the contract within 15 days of receiving them. The approval fee for condominiums is capped by Section 718.112(2)(k) at $150 per applicant, adjusted for inflation every five years. Renters are subject to the association’s governing document requirements, which vary by community, and the association may collect a security deposit capped at one month’s rent when authorized. Lender scrutiny for buyers is also increasing significantly, with Fannie Mae and Freddie Mac requiring full project reviews for nearly all condo sales starting August 3, 2026. TenantEvaluation’s intelligent form logic automatically routes buyers and renters through the correct workflow for each applicant type.

What additional requirements apply to 55+ age-restricted communities in Florida?

Florida condos and HOAs operating as 55+ communities under the Housing for Older Persons Act, or HOPA, must maintain specific documentation demonstrating that at least 80% of occupied units are occupied by at least one person 55 or older and must publish and follow policies demonstrating intent to be age-restricted housing. Application handling for these communities often involves additional eligibility documentation that must be collected, stored, and maintained consistently across all applicants. TenantEvaluation’s 55+ Communities Verification capability is built for Florida condos and HOAs and designed for Community Association Managers, and it reduces manual work, standardizes application handling, supports documentation consistency, improves operational efficiency, and strengthens internal processes without replacing legal guidance.

What does FCRA compliance mean for condo board approvals?

The Fair Credit Reporting Act governs how consumer reports, including credit, criminal background, and eviction history, are obtained and used in applicant screening. Associations and their managers must have a permissible purpose to obtain a report, certify that purpose to the consumer reporting agency, and provide required adverse action disclosures if a report contributes to a rejection decision. FCRA also requires documented policies for handling address discrepancy notices and maintaining applicant data securely. TenantEvaluation is built with FCRA compliance as the foundation and operates as a direct reseller of TransUnion and Equifax data with built-in adverse action workflows, strict permissible purpose controls, and full audit trails for every application.

Conclusion: Streamline Your Florida Condo Approval Process

A well-structured condo board approval process in Florida requires more than a document checklist. It requires consistent identity verification, FCRA-compliant screening, governing document alignment, a documented board review workflow, and clear communication at every stage. Manual processes introduce gaps at each of these points and create delays, compliance exposure, and fraud risk that accumulate over time.

The 10-step checklist in this guide provides a repeatable framework for both purchase and rental approvals. Reviewing your current process against each step will reveal where bottlenecks and compliance gaps exist. For communities ready to move beyond manual workflows, TenantEvaluation provides the infrastructure to automate, verify, and document every stage of the approval process, from application intake through final board decision.

Review how TenantEvaluation supports your approval workflow with an FCRA-first platform built for Florida communities.