Written by: Luis Teran, Co-founder, CEO, TenantEvaluation

Key Takeaways

- Florida 55+ communities rely on minimum credit scores, income verification, background checks, and HOPA 80/20 age compliance for approvals.

- Credit thresholds vary by region, with typical minimums around 590–650; low-score applicants can use co-signers, assets, or larger deposits to qualify.

- FCRA rules require written consent and clear adverse action notices, and automated platforms help communities stay compliant while cutting processing time.

- Community Association Managers benefit from tools like IDVerify for biometric checks and QuickApprove dashboards for faster, more consistent board reviews.

- Communities can streamline 55+ screening and reduce manual work by using TenantEvaluation to modernize their approval process while maintaining full FCRA compliance.

Core Credit & Background Standards for Florida 55+ Communities

Florida 55+ communities set financial and background criteria that applicants must meet before approval. Silver Bay Palatka requires applicants to demonstrate financial ability to purchase a home and pay monthly lot rent through proof of income, bank statements, or other financial documentation.

These screening components work together to show both ability and willingness to pay, along with basic safety checks.

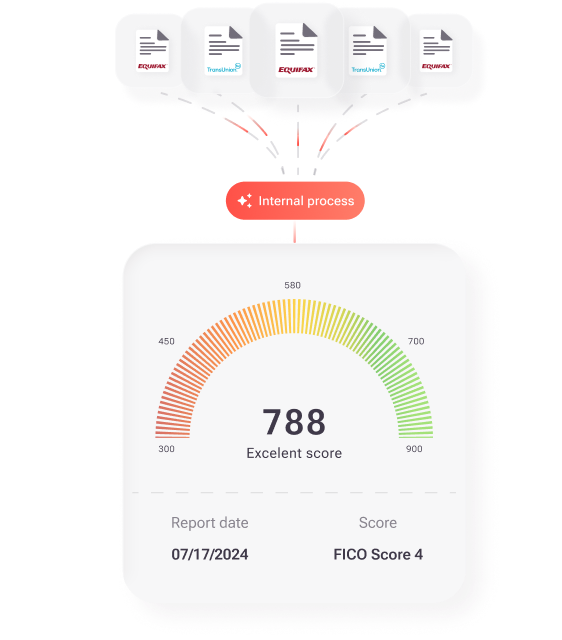

- Credit Score Requirements: Each community sets its own minimum score based on risk tolerance and local market conditions.

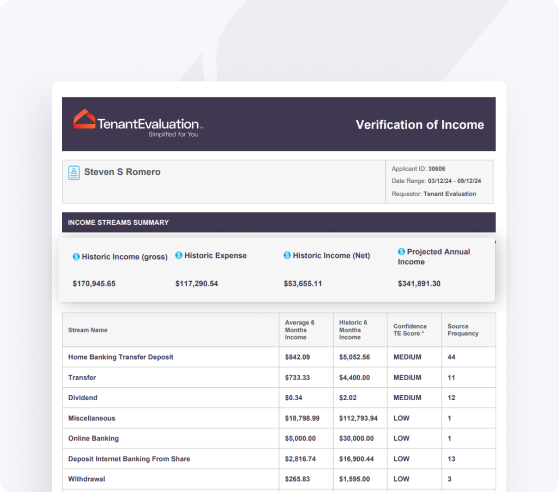

- Income Verification: Applicants provide paystubs, tax returns, or pension statements to prove they can cover monthly community fees.

- Background Checks: Communities review criminal history and eviction records to protect residents and property.

- FCRA Compliance: Written consent forms and adverse action procedures keep screening aligned with federal law.

Credit score minimums, income-to-fee ratios, and reserve requirements vary significantly by community. Typical Florida 55+ communities may accept credit scores in the 590–620 range, while stricter HOAs in competitive markets often require 650 or higher. Many communities look for monthly income at least three times the monthly fee, although some accept slightly lower ratios when applicants show strong assets or long-term retirement income.

Under the FCRA, Florida landlords must obtain written consent from applicants prior to accessing credit reports or background checks for tenant screening, which ensures proper authorization before screening begins.

Florida 55+ Rules, HOPA 80/20, and Regional Credit Trends

Beyond these universal FCRA requirements, Florida’s 55+ communities follow additional rules specific to age-restricted housing. Florida’s age-restricted communities operate under the Housing for Older Persons Act, which creates specific compliance obligations.

Credit expectations also shift by region, based on demand and local pricing.

- Miami-Dade: Higher demand often leads to stricter credit standards and higher minimum scores.

- Tampa Bay: Some communities maintain firm thresholds, while others offer more flexible options.

- Central Florida: Many communities focus on stable retirement income and long-term residency patterns.

Background checks commonly include review of criminal history and eviction records. Background checks are common in Florida 55+ communities to ensure resident safety and typically include criminal background checks and possibly credit checks.

Paths to Approval for 55+ Applicants with Low Credit Scores

Applicants with credit scores below community thresholds can still improve their approval chances through targeted steps and strong compensating factors.

Credit Improvement Steps:

Start by reviewing your credit report for errors and disputing inaccuracies through bureau channels, since removing incorrect items can raise scores quickly. While those disputes move through the system, pay down existing revolving debt to improve your credit utilization ratio, which influences your score right away. For legitimate collections or past-due accounts, set up payment plans to show that you are actively resolving issues. After taking these actions, consider rapid rescoring services before application submission so your updated information appears when the community pulls your credit.

Alternative Qualification Methods:

- Co-signers: Adult children or financially qualified relatives can co-sign applications and share responsibility.

- Larger Security Deposits: Additional deposits can help offset perceived credit risk for the community.

- Asset Documentation: Savings, retirement accounts, and investments can demonstrate strong financial reserves.

- Income Verification: Pension, Social Security, and retirement distributions provide proof of stable, ongoing income.

Applicants with lower credit scores may qualify when they present significant compensating factors and clear documentation. Lenders may require 12–24 months of reserve assets for certain loan types to retired borrowers in Florida, and some communities look for similar reserve strength when evaluating risk.

While understanding applicant qualification strategies is essential, Community Association Managers also need efficient systems to evaluate these applications consistently and compliantly.

CAM & Board Screening Best Practices with TenantEvaluation

Community Association Managers face mounting pressure to process applications quickly while maintaining FCRA compliance and consistent screening standards. Manual processes often create bottlenecks, increase compliance risk, and lead to inconsistent decisions across similar applications.

TenantEvaluation addresses these challenges through a comprehensive platform designed for Florida condos and HOAs. The system includes 55+ Communities Verification, which reduces manual work, standardizes application handling, supports documentation consistency, and improves operational efficiency for Community Association Managers.

Key platform features work together to create a single, compliant workflow from application to decision.

- FCRA Foundation: Built-in compliance workflows with automated adverse action procedures keep decisions documented and consistent.

- Direct Bureau Reseller: Direct TransUnion and Equifax data access under strict bureau rules supports accurate, timely reports.

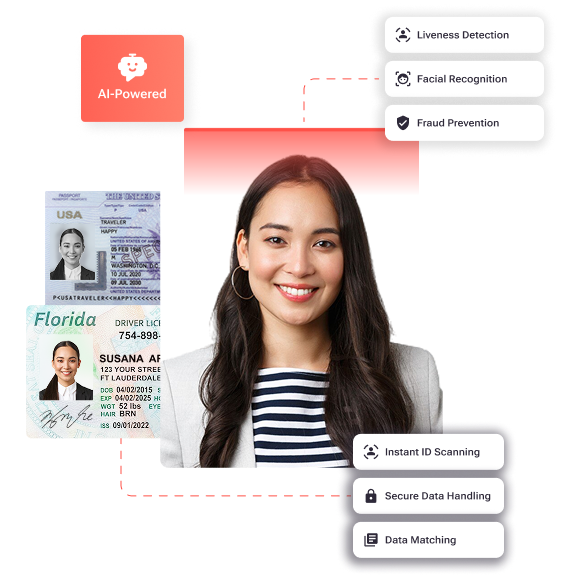

- IDVerify: Biometric identity verification prevents fraud through government ID validation and liveness detection.

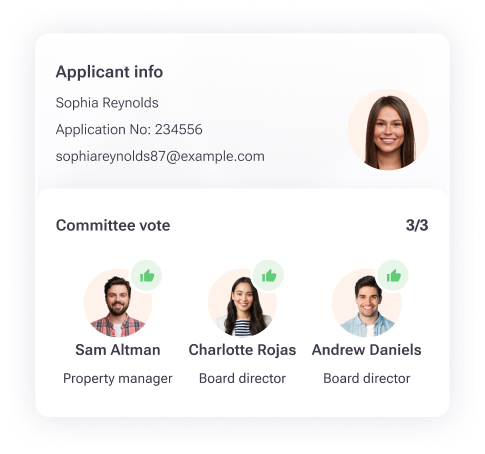

- QuickApprove: A board-specific dashboard centralizes applicant data for faster, more transparent approvals.

The following comparison illustrates how TenantEvaluation’s specialized 55+ community features deliver faster processing and better board integration than general-purpose screening services.

| Feature | TenantEvaluation | ApplyCheck/Verify Screening |

|---|---|---|

| Processing Time | 5–10 minutes per application on average | 5–10 days for many standard screenings |

| Revenue Model | Revenue sharing with no upfront platform fees, which can reduce out-of-pocket costs for communities | Pay-per-screening fees with no monthly subscriptions, which keeps costs tied to volume |

| 55+ Community Support | Built-in verification workflows tailored to age-restricted communities | General screening for HOAs and associations without 55+ specific tools |

| Board Integration | Dedicated QuickApprove dashboard for board review and voting | No board-specific tools for collaborative decisions |

TenantEvaluation serves over 5,000 communities with 100,000+ applications processed annually, delivering up to 70% time savings for property management teams. See how these time savings apply to your community’s screening volume and staffing levels.

Digital Application Workflow for 55+ Community Screening

Modern 55+ community screening now follows a structured digital process that replaces paper files and scattered emails.

- Online Application Submission: Applicants complete forms through secure web portals, which reduces data entry for staff.

- Identity Verification: IDVerify confirms applicant identity through biometric validation and document checks.

- Credit & Background Processing: Automated bureau queries run after FCRA-compliant consent, producing consistent reports.

- Income Documentation: Applicants upload financial documents digitally, and managers review them in a single system.

- Board Review: The QuickApprove dashboard presents summarized applicant data for faster, more informed decisions.

- Approval Notification: Automated communications go to applicants, managers, and boards, with a full audit trail.

This workflow reduces processing time from days to hours and keeps every step documented for future compliance audits.

Key Compliance Priorities for Florida 55+ Communities in 2026

Florida 55+ communities must track evolving FCRA requirements and fair housing regulations while they screen applicants. Under the FCRA, Florida landlords must provide a clear, written adverse action notice if denying a tenant applicant based on credit or background report information.

TenantEvaluation’s platform supports these obligations through automated adverse action workflows, built-in audit trails, and direct credit bureau relationships that help maintain data accuracy. The system’s biometric verification capabilities also strengthen identity confirmation and reduce fraud exposure in high-value community environments.

Frequently Asked Questions

What is the 80/20 rule for Florida 55+ communities?

The 80/20 rule under the Housing for Older Persons Act requires that at least 80% of occupied units in age-restricted communities have at least one resident who is 55 years or older. This allows up to 20% of units to house younger residents, though individual communities may adopt stricter 100% age requirements. The rule enables communities to qualify for Fair Housing Act exemptions while maintaining flexibility for younger spouses or adult children living with qualifying residents.

What is the lowest credit score that can qualify for a 55+ community in Florida?

Florida 55+ communities set their own minimum credit score requirements, but many follow similar ranges. Typical thresholds fall around 590–600 statewide, with higher ranges such as 620–650+ in Miami, 590–620 in Tampa, and 600–620 in Orlando. Some communities accept lower scores when applicants show strong compensating factors like substantial asset reserves, co-signers with strong credit, larger security deposits, or stable retirement income.

Can someone with a low credit score qualify for a 55+ community?

Applicants with lower credit scores may qualify when they present exceptional compensating factors. These can include co-signers with excellent credit, substantial cash reserves, significant asset documentation, larger security deposits, or proof of stable pension or Social Security income. Each application is evaluated individually based on the community’s specific criteria and risk tolerance.

Does an eviction automatically disqualify someone from a 55+ community?

Evictions do not automatically disqualify applicants, but they can reduce approval chances. Communities typically evaluate the circumstances, timing, and resolution status. Evictions followed by several years of stable housing may be acceptable. Some communities allow explanatory letters or require co-signers for applicants with eviction history. The key factors include the reason for the eviction and subsequent rental performance.

Are Florida 55+ communities required to accept families with children?

No, qualified 55+ communities in Florida are exempt from familial status protections under the Fair Housing Act when they meet specific criteria including the 80/20 age rule and proper documentation. These communities can legally refuse applications from families with children under 18. However, they must allow younger spouses and adult children over 18 to reside with qualifying 55+ residents. Communities must maintain proper documentation and registration to preserve this exemption status.

Conclusion

Florida’s 55+ community credit check requirements call for careful preparation from applicants and systematic compliance from Community Association Managers. Clear credit thresholds, income documentation standards, and HOPA age verification rules support successful applications while protecting communities from regulatory risk.

TenantEvaluation’s specialized platform turns manual screening into automated, FCRA-compliant workflows tailored to Florida’s age-restricted communities. With 55+ Communities Verification, biometric identity confirmation, and board-specific approval tools, the system delivers the time savings described earlier while strengthening operational control. Explore how TenantEvaluation streamlines 55+ community screening while maintaining comprehensive compliance and documentation consistency.