Written by: Luis Teran, Co-founder, CEO, TenantEvaluation

Key Takeaways for Florida HOA Screening

- Rental fraud now affects 93% of landlords, up 40% since 2023, so Florida HOAs must tighten screening to avoid evictions and liability.

- Verify income beyond self-reports and watch for income below 3x rent, unverifiable employment, and high debt-to-income ratios.

- Track behavioral red flags such as rushed applications or badmouthing landlords, along with eviction records and relevant criminal history.

- Catch document fraud through fake paystubs, SSN mismatches, and biometric failures using AI liveness detection.

- Maintain FCRA compliance with standalone disclosures and consistent standards, and get started with TenantEvaluation for automated, fraud-resistant tenant screening.

Financial Red Flags: Verify Income Beyond Self-Reports

Flag 1: Income Below 3x Rent

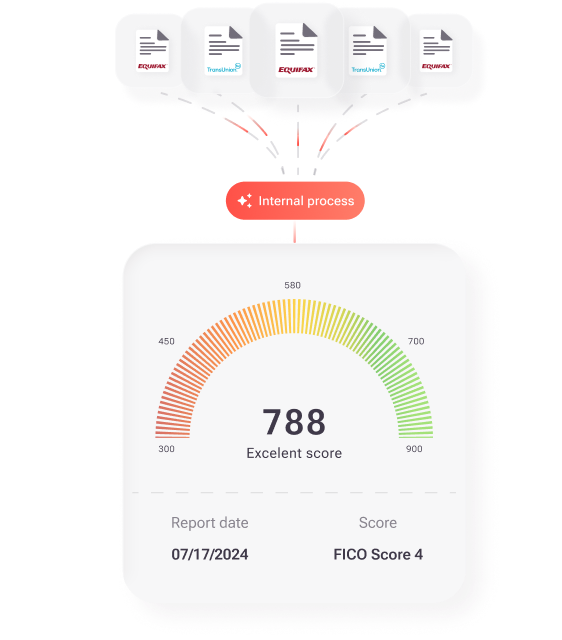

Most communities require applicants to earn 2.5 to 3 times the monthly rent in gross income. When applicants fall below this threshold, the risk of nonpayment and bad debt rises sharply. Approximately 25% of bad-debt losses can be traced back to fraud that slipped through the approval process, often involving inflated or falsified income documentation. Verify income through direct payroll connections and bank data instead of relying on easily altered pay stubs.

| Monthly Rent | Minimum Income (3x) | Risk Level if Below |

|---|---|---|

| $2,000 | $6,000 | High eviction risk |

| $3,000 | $9,000 | Moderate risk |

| $4,000 | $12,000 | Low risk if verified |

Flag 2: Unverifiable Employment

Unverifiable employment details signal a high likelihood of falsified income. AI-generated employment verification letters now mimic real company letterhead and signatures with alarming accuracy. Always confirm employment through publicly listed phone numbers or trusted databases instead of applicant-provided contacts. TenantEvaluation’s IncomeEv reports go beyond self-reported data by contacting employers directly, which removes most document manipulation risks.

Flag 3: High Debt-to-Income Ratios

High existing debt relative to income often predicts payment difficulties, even when applicants technically meet income minimums. When you review credit reports to assess debt-to-income ratios, you trigger federal rules that govern what information can appear. The FCRA imposes strict limits on reportable information in criminal background checks, including a seven-year lookback rule for arrests that also applies to most negative credit items used in rental decisions. Work with screening tools that apply these limits consistently so your board avoids using outdated or non-compliant data.

Behavioral Red Flags: Watch for Aggression in HOA Meetings

Flag 4: Rushing Process or Cash Offers

Applicants who push for immediate approval or offer cash payments often try to hide eviction histories or other disqualifying issues. This urgency can pressure board members to skip steps or shorten review timelines. Document any attempts to bypass standard procedures and insist on completing full screening before granting access to the property.

Flag 5: Badmouthing Previous Landlords

Frequent complaints about previous landlords, neighbors, or associations often foreshadow future disputes with your HOA board or management company. These patterns may indicate difficulty following community rules or resolving conflicts calmly. Record these comments during interviews so the board can weigh behavioral risk alongside financial and background data.

Background Red Flags: Eviction History in Florida

Flag 6: Eviction Records

Nearly one in four eviction filings over the past three years involved a tenant who had submitted a fraudulent rental application. This pattern shows how often applicants hide prior problems when seeking approval. Florida’s streamlined eviction process moves quickly, so boards need clear documentation of screening decisions to defend against discrimination claims. Track how eviction history influenced each decision and apply the same standards to every applicant.

Flag 7: Criminal History (Violence or Fraud)

Criminal history that involves violence, property damage, or fraud directly affects community safety and asset protection. Focus on offenses that relate to resident security, financial integrity, and rule compliance instead of minor or unrelated issues. Keep in mind the seven-year reporting limit described earlier and align your criteria with both FCRA rules and fair housing guidance.

Document Fraud Red Flags: Biometric Fails Surge 30% in FL HOAs

Flag 8: Fake Paystubs and IDs

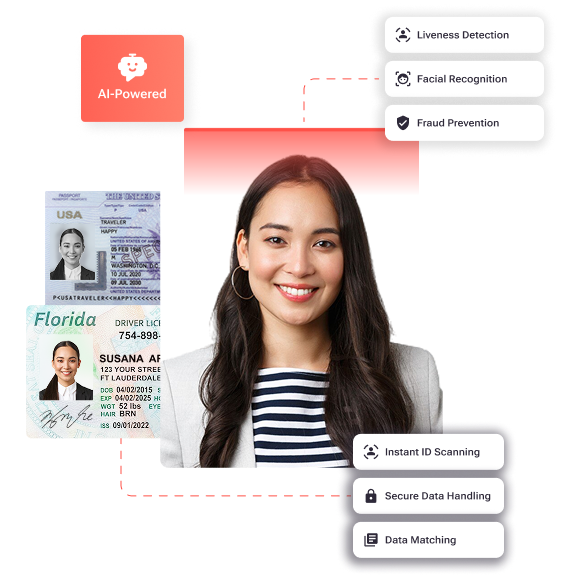

Fraud packages sold on social media like TikTok now include fabricated income documentation, alternative identification numbers, counterfeit employment verification on realistic-looking letterhead, altered banking records showing inflated balances, and template-generated pay stubs. These kits help applicants defeat basic document checks. TenantEvaluation’s IDVerify uses AI-powered liveness detection and ID validation to confirm that documents match a real, present person instead of a stolen or synthetic identity.

Flag 9: SSN Hesitation or Mismatches

Hesitation to provide a Social Security number or repeated corrections often points to identity concerns. Mismatches between the SSN on the application and the number tied to the credit report suggest identity theft or synthetic identity fraud. Treat these discrepancies as serious red flags and pause approvals until you resolve the conflict with verified data.

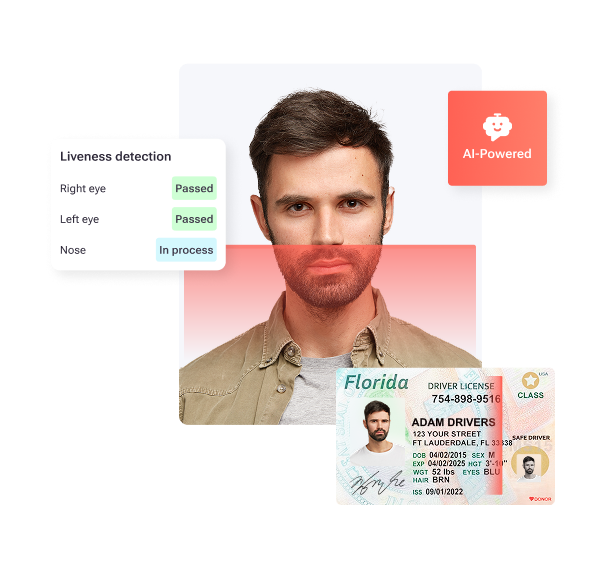

Flag 10: Inconsistent Selfies

Selfies that do not match government ID photos or fail biometric checks frequently indicate attempts to use stolen identities. Biometric verification failures also appear when applicants submit manipulated or filtered images that distort key facial features. Liveness detection technology confirms that a real person is present during submission and that the face matches the ID on file.

Compliance Red Flags: Avoid FCRA Traps in Florida HOAs

Florida HOAs operate under specific legal and financial constraints that can weaken screening programs. Florida condominium associations cannot charge fees for lease or sublease approvals unless the documents require such approval and authorize the fee, and the fee is capped at $150 per applicant. This fee cap limits how much boards can invest in screening and often slows approvals when boards rely on manual review. The combination of tight budgets and approval delays gives fraudsters more time to exploit gaps in manual processes.

Flag 11: No Standalone FCRA Disclosure

The Fair Credit Reporting Act (FCRA) requires a standalone written disclosure and written authorization from the candidate before running any criminal background check for housing or employment decisions. Embedding consent language inside a long rental application or community packet violates this requirement. Use a clear, separate disclosure and authorization form for every applicant and keep records of signed approvals.

Flag 12: Uneven Screening Standards

Inconsistent application of screening criteria exposes HOAs to discrimination and fair housing claims. Checkr’s 2024 survey found that 47% of organizations lack confidence in their screening compliance, which often stems from ad hoc decisions. Standardized, automated processes apply the same rules to every applicant, reduce bias, and create a clear audit trail for board decisions.

Secure Screening Starts Here: TenantEvaluation’s FCRA-First Platform

TenantEvaluation processes more than 100,000 applications each year for over 5,000 communities, generating $150 million for communities while cutting screening time by up to 70%. Unlike competitors that depend on third-party redirects, TenantEvaluation’s end-to-end platform integrates IDVerify biometric verification and the QuickApprove board dashboard in a single environment.

As a direct TransUnion and Equifax reseller with PCI Level 1 compliance, TenantEvaluation treats FCRA compliance as the foundation of every workflow. Automated adverse action tools and built-in audit trails protect Florida HOAs from regulatory violations while keeping board approvals moving quickly.

Unlike ApplyCheck’s reliance on TazWorks, TenantEvaluation’s proprietary automation blocks fraud at the source through biometric identity verification, automated document redaction, and real-time verification. No external logins or disconnected systems are required. Schedule a demo today to see how leading Florida property management companies protect their communities.

FAQ: Secure Tenant Screening for Florida HOAs

What are FCRA red flags in tenant screening?

FCRA red flags include missing standalone written disclosures before screening, skipping adverse action procedures when denying or conditioning applications, and using screening providers that ignore federal rules. The seven-year lookback rule limits which criminal and credit items can appear in reports used for most rental decisions. Automated adverse action workflows help boards send proper notices, while separating data providers from decision-makers keeps compliance responsibilities clear.

What are biometric fraud signs in rental applications?

Biometric fraud signs include inconsistent facial features between submitted photos, repeated failed liveness detection tests, and government ID photos that do not match the applicant’s selfie. Advanced fraudsters now use deepfake tools and stolen identities to bypass basic document checks. IDVerify technology combines government ID validation, AI-powered liveness detection, and facial landmark recognition to confirm applicant authenticity in real time.

What eviction history red flags should Florida HOAs watch for?

Florida HOAs should flag multiple eviction filings, recent evictions for nonpayment, and unexplained gaps in rental history that may hide prior evictions. Fraudulent applications often omit previous addresses or list fake landlords to conceal court records. Cross-reference stated rental history with court databases and contact previous landlords using independently sourced phone numbers instead of applicant-provided details.

How do Florida HOA fee caps affect screening security?

Florida’s $150 fee cap for condominium associations restricts how much boards can spend on each application, which limits some screening options. This constraint forces associations to balance thorough verification with cost compliance and can leave gaps that fraudsters exploit. TenantEvaluation’s revenue-sharing model creates a cost-neutral or revenue-generating approach while still delivering comprehensive screening within regulatory limits.

What income verification methods prevent rental fraud?

Effective income verification connects directly to payroll providers and bank accounts instead of relying on uploaded documents alone. Automated systems review deposit patterns, confirm employer details, and detect document tampering through OCR and data-matching technology. Real-time verification shortens the window that fraudsters use to submit fake pay stubs or edited bank statements.

Your Secure Screening Checklist: Next Steps for Florida HOAs

Use this checklist to spot 12 key red flags when screening rental applicants securely:

- Income below a 3x rent ratio

- Unverifiable or suspicious employment details

- High debt-to-income ratios

- Rushed application timelines or cash offers

- Negative or hostile landlord references

- Eviction history patterns or hidden filings

- Relevant criminal records tied to safety or fraud

- Fake or altered documents in the application

- Social Security number inconsistencies

- Failed or inconsistent biometric verification

- Missing or improper FCRA disclosures

- Inconsistent screening standards across applicants

Protect your Florida HOA from the 40% surge in rental fraud with TenantEvaluation’s comprehensive screening platform. The FCRA-compliant system combines biometric verification, automated compliance workflows, and board-specific dashboards to close manual screening gaps. Schedule a demo today to secure your community’s screening process.