Written by: Luis Teran, Co-founder, CEO, TenantEvaluation

Key Takeaways

- Florida has a severe shortage of FHA-approved condos, with only 0.9% of South Florida inventory eligible, which creates financing bottlenecks for property managers.

- FHA approval requires at least 50% owner-occupancy, no more than 15% delinquency, at least 10% reserves, and proper insurance, while Florida faces added pressure from SB 4-D and higher down payment rules.

- Property managers can use HUD’s condo lookup tool to verify status by state, county, or ZIP, and must track three-year expirations and spot approvals for individual units in non-approved projects.

- Expired approvals, insurance gaps from Florida’s crisis, and manual workflows often slow resident onboarding and disrupt financing.

- Automating FHA checks and screening with TenantEvaluation streamlines approvals, supports FCRA compliance, and increases revenue for Florida communities.

Why Florida Property Managers Rely on the FHA Approved Condo List

The Florida condo crisis intensified after the 2021 Surfside collapse and the regulatory changes that followed. FHA-approved condo projects in South Florida have declined sharply as associations struggle to meet updated insurance coverage and reserve funding requirements under SB 4-D. Property managers now must locate the shrinking pool of FHA-eligible properties while keeping up with more complex compliance rules.

Manual FHA verification creates serious operational slowdowns. When property managers skip FHA checks at the start of screening, applications often stall for weeks while associations chase spot approvals or uncover financing limits. These delays reduce revenue and hurt resident satisfaction. The pressure is higher in Florida’s competitive rental market, where condo values have slipped 9.9% over the past 12 months because of ongoing market distress.

Core FHA Rules and How They Apply in Florida

FHA condo approval requires each condominium project to meet strict federal guidelines recorded in HUD’s official database at HUD’s condo lookup tool. FHA single-unit condo approval standards require at least 50% owner-occupied units, no more than 15% of units delinquent on dues, and the condo association holding at least 10% of the HOA budget in cash reserves.

Florida adds several layers of complexity that affect FHA eligibility. FHA appraisals for Florida condominiums focus on structural soundness, roofs with at least two years of remaining life, and termite damage, which is a major concern in the state. In addition, Florida is the only U.S. state that requires a 25% down payment for a limited review when the condo building lacks sufficient reserves, compared to 10% in every other state.

| Requirement | Threshold | Florida Note |

|---|---|---|

| Owner-Occupancy | ≥50% | Tracked annually |

| Delinquency Rate | ≤15% | 60+ day delinquencies |

| Reserve Fund | ≥10% of budget | SB 4-D compliance required |

| Insurance Coverage | HUD minimums | Hurricane and flood coverage are critical |

2026 FHA Trends, Spot Approvals, and Florida Condo Pressures

Only an estimated 6.5% of the roughly 150,000 condo projects in the U.S. are currently FHA-approved, and Florida represents a small share of that total. The three-year recertification cycle means many projects that once qualified have now expired without renewal. This pattern creates more demand for spot approvals on individual units.

Property managers increasingly depend on single-unit spot approvals when entire projects lack FHA certification. A 2019 FHA rule change allowed individual condo units to receive approval separately, while earlier rules required full community approval. Spot approvals, however, require extensive documentation and often take 30 to 60 days to process, which slows resident onboarding and complicates move-in timelines.

The insurance crisis mentioned earlier compounds these challenges. Many insurance carriers have withdrawn from Florida’s condo market due to spiking climate risks, which makes it harder for associations to maintain the coverage levels FHA requires. Talk with our team to see how TenantEvaluation’s automated workflows help property managers handle these pressures.

Step-by-Step HUD FHA Condo Lookup for Florida Property Managers

How to Check if a Condominium Is FHA-Approved in Florida

Property managers can follow this systematic approach to verify FHA status and keep applications moving.

1. Access HUD’s Official Database: Navigate to HUD’s condo lookup tool using any internet browser. This database is the only authoritative source for current FHA condo approval status.

2. Enter Search Criteria: Once in the tool, input state, county, condo ID, condo name, city, or ZIP code. Fewer details return more results, which helps when you are unsure of the exact project name or spelling.

3. Review Status Information: Check the status section for “Approved,” “Rejected,” “Expired,” or “Withdrawn” designations. An approved label alone is not enough, because approvals can expire and leave buyers without FHA options.

4. Verify Expiration Dates: HUD FHA condo project approvals are generally valid for three years, and the HOA must reapply to HUD to keep approval active. If the expiration date is near or already passed, the project may lose eligibility during a buyer’s loan process.

5. Document Results: Save screenshots and approval numbers for resident files and board documentation. This record protects the association and the manager if FHA status changes while an application is in progress.

FHA Loans on Florida Condos and Single-Unit Paths

Florida buyers can obtain FHA loans on condos, but eligibility depends on project approval status or single-unit approval routes. For condominium units in non-FHA-approved projects, the FHA permits single-unit approvals on a case-by-case basis, where an FHA-approved lender works with the HOA or property management to file required paperwork.

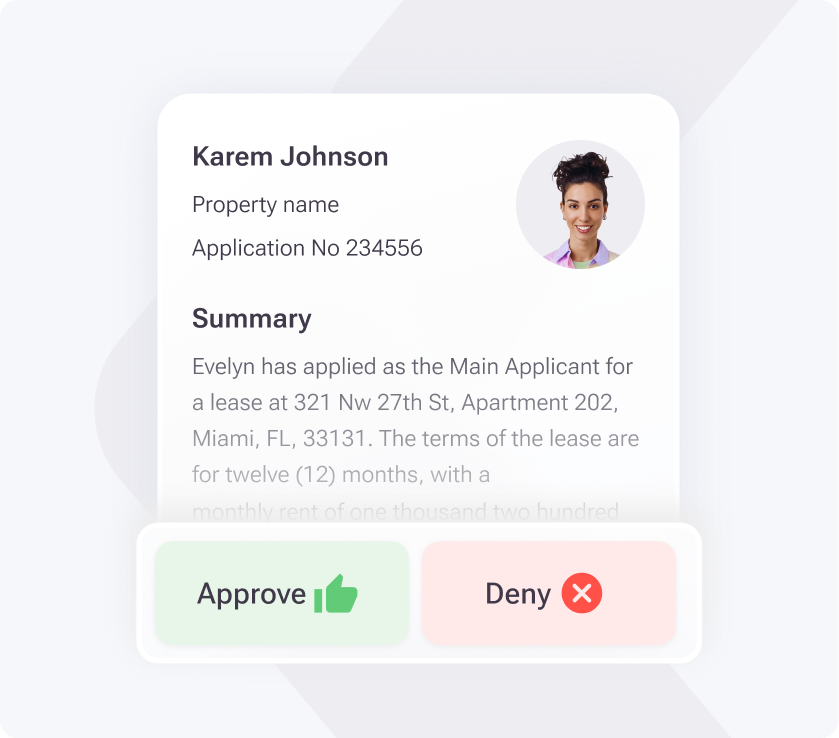

Property managers should build FHA verification into their initial screening workflows to avoid financing delays later. TenantEvaluation’s platform supports efficient screening, which allows CAMs to redirect prospects toward suitable financing or start spot approval procedures early. See how automated resident onboarding works and how it fits into your current process.

Common FHA Verification Pitfalls for Florida CAMs

Florida property managers face several recurring obstacles when they manage FHA verification. Expired approvals are the most frequent problem, because many associations do not track three-year recertification deadlines. When approvals lapse, units that once qualified suddenly lose access to FHA financing, which can derail pending applications and closings.

Confusion between project approval and single-unit approval creates further complications. Many property managers assume that individual units can always qualify for spot approval. However, single-unit spot approvals require the project to meet the reserve thresholds outlined earlier, demonstrate adequate insurance, avoid FHA-restricted status, and show no litigation that affects marketability or safety.

Insurance coverage gaps create particular challenges in Florida’s volatile market. Growing numbers of South Florida condo buildings are losing “warrantable” status under Fannie Mae and Freddie Mac because of inadequate insurance, underfunded reserves, and low owner-occupancy ratios. These same weaknesses affect FHA eligibility and create cascading financing restrictions for buyers and residents.

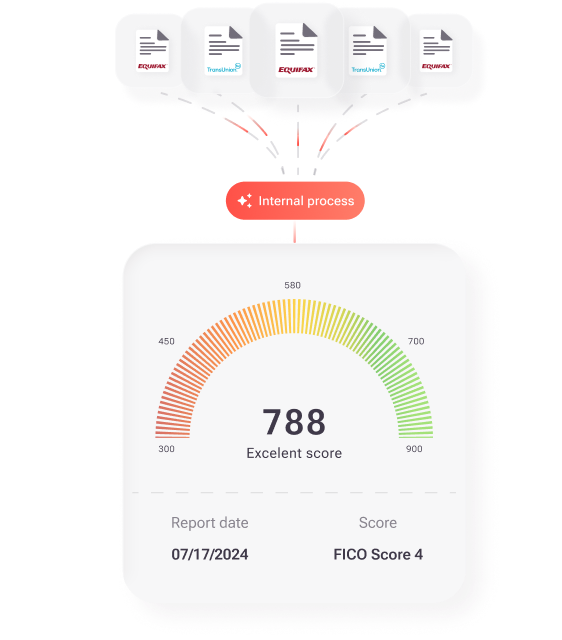

Manual verification processes make these issues worse by adding delays and compliance risks. Property managers who handle sensitive applicant data without strong FCRA protocols face potential liability, especially when FHA verification involves credit and financial information.

Automating FHA Checks and Resident Screening with TenantEvaluation

TenantEvaluation turns manual resident screening and onboarding into an automated workflow for community associations and management companies. The platform includes Florida-specific configuration that supports SB 4-D tracking and other state requirements.

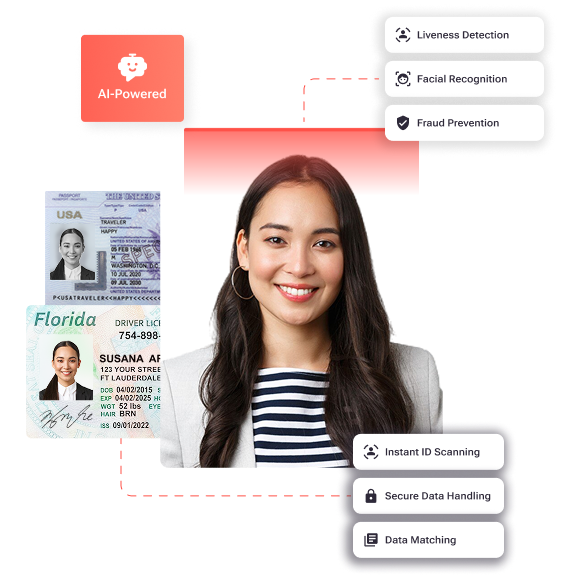

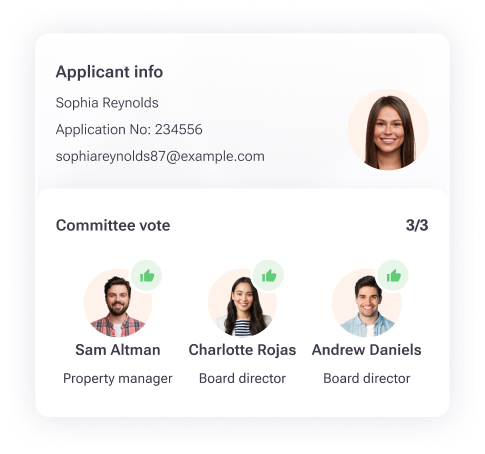

Unlike competitors that focus only on background screening, TenantEvaluation delivers full resident onboarding with FCRA compliance at the core. The platform integrates the QuickApprove dashboard for board oversight and IDVerify biometric verification to reduce fraud risk throughout screening.

TenantEvaluation has generated more than $150 million for communities while serving over 5,000 properties and maintaining a 4.8 out of 5 Google rating. Property managers report time savings of up to 70% compared with manual processes.

The following comparison table highlights how TenantEvaluation’s integrated, Florida-focused approach differs from competitors that rely on third-party tools and generic platforms.

| Feature | TenantEvaluation | ApplyCheck | Verify Screening |

|---|---|---|---|

| Board Dashboard | QuickApprove included | Not available | Not available |

| Biometric Verification | IDVerify native | Third-party only | Third-party only |

| Florida Customization | Built-in compliance | Generic platform | Generic platform |

The platform’s revenue-sharing model aligns TenantEvaluation’s success with client outcomes and avoids heavy subscription fees. Property managers pay per application with no upfront costs, which keeps the solution accessible for communities of all sizes. Start streamlining your resident screening workflow with an introductory demo.

FAQ: FHA Condo Approval for Florida Property Managers

How do I check if a condominium is FHA-approved in Florida?

Use HUD’s official condo lookup database at entp.hud.gov/idapp/html/condlook.cfm. Enter the property’s state, county, and either the condo name, city, or ZIP code. The database then displays current approval status, expiration dates, and any restrictions. For expired or rejected projects, contact the association to ask about renewal plans or single-unit spot approval options.

Why is a condo not FHA-approved?

Common reasons include owner-occupancy below 50%, delinquency rates above 15% of units, reserve funds below 10% of the budget, or weak insurance coverage. Ongoing litigation or failure to complete recertification also cause denials. In Florida, hurricane insurance gaps and SB 4-D compliance issues frequently trigger approval lapses.

What is the FHA condo approval process for property managers?

Property managers usually coordinate with condo associations to submit documentation to HUD, including financial statements, insurance policies, governing documents, and reserve studies. The process often takes 30 to 90 days for new approvals or renewals. Single-unit spot approvals require similar documentation but focus on the individual unit’s eligibility instead of full project certification.

How often do FHA condo approvals expire?

FHA condo project approvals expire every three years and require recertification to keep eligibility. Associations must resubmit updated financial documents, insurance policies, and compliance certifications. Property managers should track expiration dates closely to avoid financing disruptions during renewals.

Can individual condo units get FHA approval if the project is not approved?

Individual condo units can qualify through single-unit spot approval processes introduced in 2019. Units must meet criteria that include adequate project reserves, proper insurance coverage, no pending litigation that affects the unit, and compliance with owner-occupancy requirements. Spot approvals require more documentation and longer processing times than project-level approvals.

Conclusion: Faster FHA Checks and Onboarding for Florida Condos

Florida property managers who master the FHA approved condo list gain faster approvals and fewer surprises during financing. Teams that embed FHA checks into automated screening workflows reduce administrative work and protect revenue. TenantEvaluation’s platform turns complex FHA verification into a clear, repeatable onboarding process that fits Florida’s 2026 market conditions. Discover how automated FHA integration can accelerate your community’s resident approval process and support your CAM team.