Written by: Luis Teran, Co-founder, CEO, TenantEvaluation

Key Takeaways for Florida HOA Fraud Protection

- Florida HOAs face rising fraud risks in 2026, with D&O insurance premiums increasing 10-15% due to governance scrutiny and legal costs.

- Five essential CAI-recommended fraud insurance options include Crime/Fidelity Bonds ($1M+), D&O, Cyber Fraud, EPLI, and Property Crime coverage.

- Florida Statute 720.3033 requires fidelity bonds equal to the maximum funds in custody, covering officers and anyone who disburses funds.

- Biometric identity verification and advanced screening tools like IDVerify+ block fake applicants before they enter communities.

- Combining insurance with TenantEvaluation's platform creates stronger protection, so schedule a demo today to reduce claims and safeguard reserves.

Five Fraud Insurance Coverages Florida HOAs Should Prioritize in 2026

Florida associations need several types of insurance to guard against fraud, embezzlement, and financial crimes. The five CAI-aligned fraud coverages below form the core of a modern protection plan.

| Coverage Type | Coverage Limits | 2026 FL Average Premium | Key Providers |

|---|---|---|---|

| Crime/Fidelity Bonds | $1M+ / $5K-$20K deductibles | $3,500-$8,000 | Amwins, Atlas, Kevin Davis |

| Directors & Officers | $2M+ / Varies | $5,000+ | Atlas, Amwins |

| Cyber Fraud Coverage | Varies / $1K-$10K | $2,000-$8,000 | Amwins, Specialty carriers |

| EPLI | $1M-$2M / $2.5K-$10K | $1,500-$4,000 | Multiple carriers |

1. Crime Insurance/Fidelity Bonds: This coverage protects against theft, embezzlement, and fraudulent transfer of association funds by employees, board members, or management companies. Typical limits range from $1 million to $5 million, with deductibles between $5,000 and $20,000.

2. Directors & Officers (D&O) Insurance: This policy shields board members from personal liability tied to management decisions and alleged wrongful acts. Premiums are increasing 10-15% in 2026 due to closer governance scrutiny and higher legal expenses.

3. Cyber Fraud Coverage: This coverage addresses ransomware attacks, wire fraud, social engineering scams, and data breaches that target association systems and financial accounts.

4. Employment Practices Liability Insurance (EPLI): This policy covers claims involving wrongful termination, discrimination, and harassment related to association employees or contractors.

5. Property Crime and Third-Party Coverage: This protection focuses on contractor fraud, vendor embezzlement, and theft by service providers who have access to association property.

Florida HOA Fidelity Bond Rules Under Statute 720.3033

Florida Statute 720.3033(5) requires homeowners associations to maintain insurance or fidelity bonds for all people who control or disburse association funds. This group includes anyone authorized to sign checks along with the association president, secretary, and treasurer.

Key requirements include:

- Coverage must equal the maximum funds in custody at any time.

- The association must pay the cost of the insurance or bond.

- Members can waive the requirement annually by majority vote at a properly called meeting.

- The rule applies to association officers and management company personnel who handle funds.

Recent Florida law changes have pushed associations toward higher insurance limits, including stronger fidelity coverage. High-profile fraud cases and post-Surfside regulatory pressure have accelerated this shift.

Steps for Reporting HOA Fraud in Florida

Associations should act quickly when fraud appears. Boards should notify the full board, the association's insurance carrier, and local law enforcement as soon as possible.

Some cases also require reports to the Florida Attorney General's office and the Department of Business and Professional Regulation (DBPR). Detailed audit trails, bank records, and internal documentation support both insurance claims and any legal action.

Prevention still offers the strongest protection. Advanced screening technology can identify and block fraudulent applicants before they gain access to communities, which lowers the risk of internal fraud and protects association assets.

Five Tech-Driven Fraud Prevention Strategies for Florida Associations

Insurance covers financial losses after fraud occurs, while prevention technology reduces the chance of fraud in the first place. The strategies below work alongside your policies to lower claims and protect reserves.

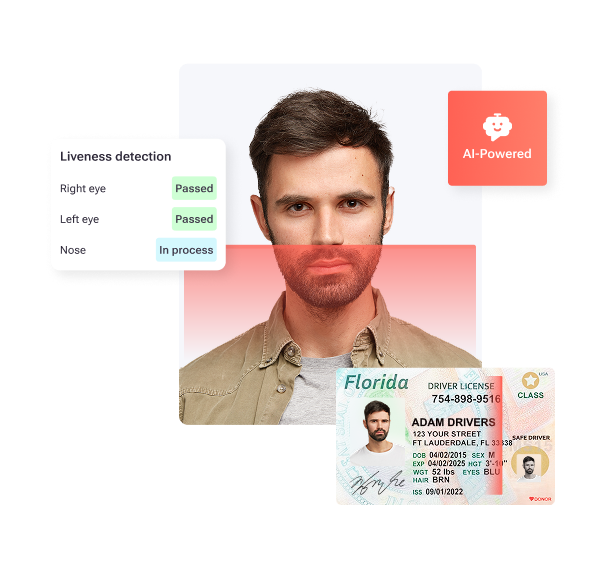

1. Biometric Identity Verification (IDVerify+): Advanced KYC verification uses government ID validation, AI-powered liveness checks, and biometric facial matching to stop identity fraud during the application process.

2. All-in-One FCRA-Compliant Platform: TenantEvaluation builds Fair Credit Reporting Act compliance into every step and maintains complete audit trails for each application.

3. Board-Specific Dashboard: QuickApprove gives board members real-time visibility into applications, AI-generated summaries, and streamlined voting tools. This setup reduces email exposure and improves oversight.

4. Automated Document Security: Automatic redaction and encryption of sensitive personal data reduce breach risks and support PCI Level 1 compliance throughout the screening workflow.

5. Revenue Generation: TenantEvaluation has generated $150 million for communities, processing more than 100,000 applications each year.

| Feature | TenantEvaluation | ApplyCheck/Verify | Buildium |

|---|---|---|---|

| Biometric Verification | Native IDVerify+ | Background-only | None |

| Board Dashboard | QuickApprove | No | Limited |

| Time Savings | 70%/50 hrs/day | Manual processes | Partial automation |

TenantEvaluation's layered approach has helped associations block fraudulent applications and protect reserves while maintaining a 4.8/5 Google rating. The biometric verification layer creates strong protection against synthetic identities and stolen ID fraud. Schedule a demo today to see how prevention technology can support your insurance strategy.

Florida HOA Fraud and Insurance: Common Questions Answered

What is the minimum fidelity bond requirement for Florida HOAs?

Florida Statute 720.3033 requires fidelity bond coverage equal to the maximum amount of association funds that will be in custody at any one time. Associations with large reserves often need $1 million or more in coverage.

The exact limit depends on cash flow, reserve balances, and operating accounts. Associations can waive this requirement each year through a majority vote, yet most insurance professionals and CAI still recommend maintaining coverage because fraud risks continue to rise.

Does biometric identity verification replace the need for fraud insurance?

Biometric verification such as IDVerify+ works alongside fraud insurance rather than replacing it. Insurance provides financial recovery after fraud, while biometric tools prevent many fraudulent applicants from entering your community.

This layered model reduces overall fraud exposure and the number of potential claims. Strong prevention technology combined with comprehensive insurance coverage offers more complete protection for association assets.

Who are the top fraud insurance providers for Florida associations?

Leading providers include Amwins, Atlas Insurance, and Kevin Davis Insurance Services, which focus on community association coverage. These carriers understand Florida regulations and design policies for HOAs and condominiums.

Boards should review each provider's claims handling record, policy customization options, and knowledge of association operations. Pairing a strong carrier with prevention technology like TenantEvaluation's platform gives associations broader protection.

What are the 2026 premium trends for association fraud insurance?

Premiums continue to rise across fraud-related coverages, with D&O insurance showing 10-15% increases in 2026. Crime and fidelity bond premiums have also climbed due to more frequent claims and larger losses.

Associations that use advanced fraud prevention technology often qualify for better pricing because they present a lower risk profile. Prevention tools can help offset premium increases by showing insurers clear, proactive risk management.

How can associations reduce their fraud insurance costs?

Associations can lower costs by combining strong fraud prevention, disciplined internal controls, and documented risk management practices. TenantEvaluation's biometric verification and screening platform signals to insurers that the board takes fraud seriously.

Regular board training, segregation of financial duties, and written procedures also support better rates. Insurers respond favorably when associations show they work to prevent fraud instead of relying only on coverage after losses.

Protect Your Florida Association with Insurance and Prevention Technology

Florida associations face complex fraud threats that require both comprehensive insurance coverage and proactive prevention. The five CAI-aligned insurance options, including crime and fidelity bonds, D&O coverage, cyber fraud protection, EPLI, and property crime coverage, provide essential financial backup when fraud occurs.

The strongest strategy combines that coverage with advanced prevention tools. TenantEvaluation's biometric identity verification, FCRA-compliant screening platform, and board-focused dashboard create multiple layers of defense that reduce fraud exposure before it reaches your community.

With more than 5,000 communities served and $150 million generated for associations, TenantEvaluation offers fraud prevention technology that fits modern insurance programs. Schedule a demo today to see how biometric verification and automated screening can protect your association's reserves while simplifying daily operations.